Audio By Carbonatix

More than half of the record GH¢5.2 billion in financial irregularities recorded across Ghana's ministries, departments and agencies in 2025 stemmed not from procurement breaches or payroll anomalies, but from unpaid taxes owed by just ten state institutions.

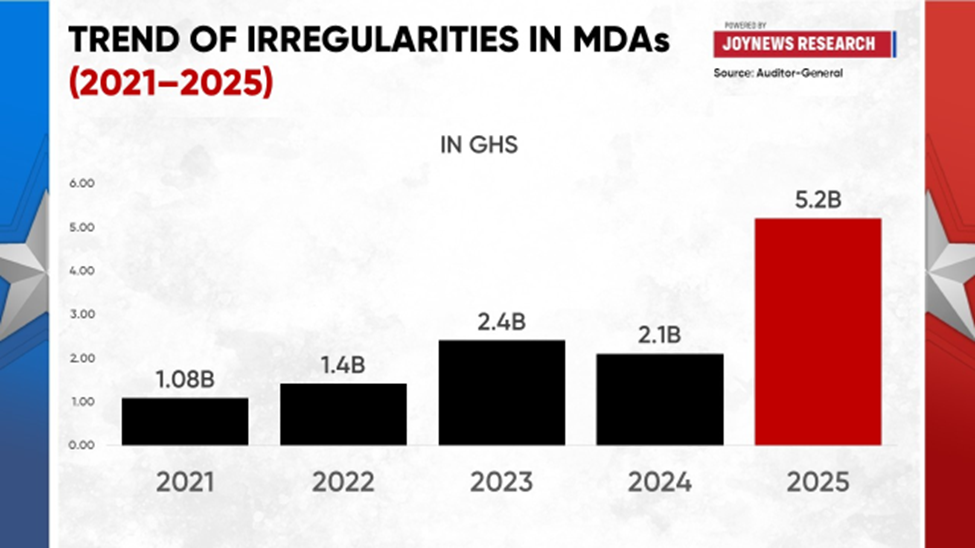

According to the Auditor-General's latest report on the public accounts of government ministries, departments and agencies, total irregularities reached GH¢5.2 billion in 2025, the highest level recorded since at least 2021.

The figure represents an increase of more than 156% compared with the previous year and is more than three times the average annual irregularities recorded over the past five years.

The sharp increase was overwhelmingly driven by tax irregularities.

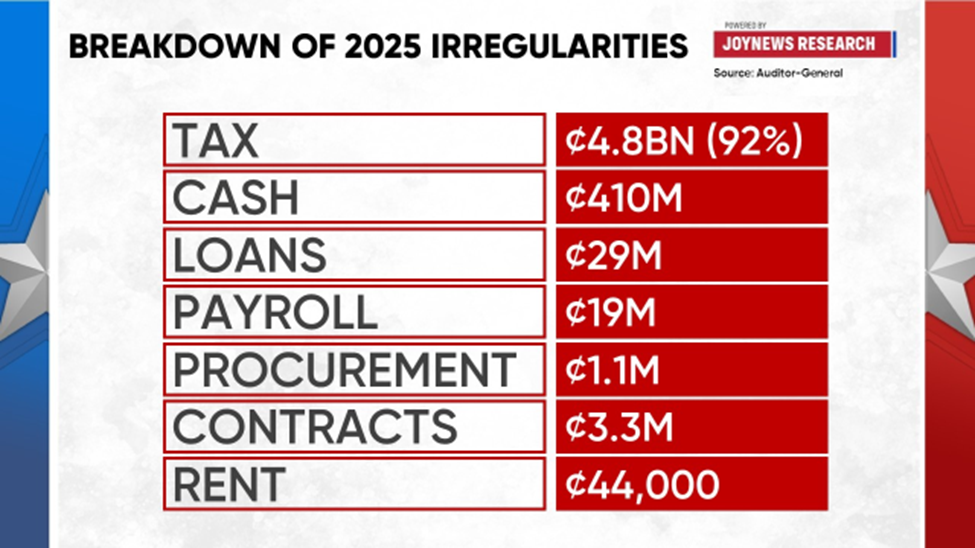

According to the report, tax related irregularities totaled approximately GH¢4.8 billion, accounting for about 92% of all irregularities identified during the audit.

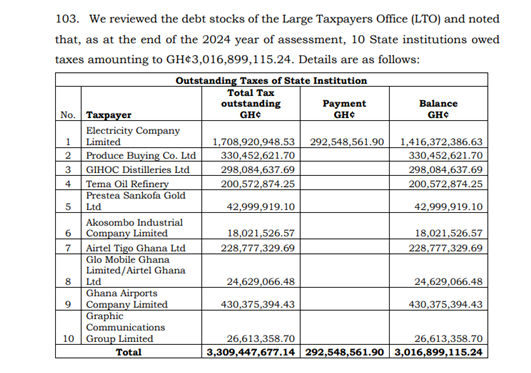

More significantly, over GH¢3 billion of those tax irregularities relate to outstanding tax obligations accumulated by ten state institutions during 2024.

In other words, more than half of all the irregularities reported in the Auditor-General's 2025 report actually originated from taxes that were due the previous year but had not been remitted.

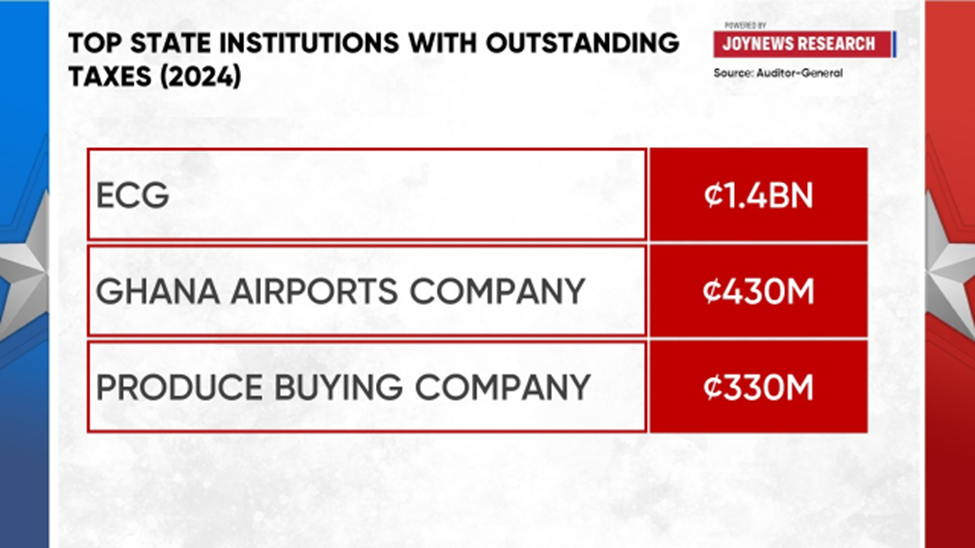

The Electricity Company of Ghana accounted for the single largest outstanding liability.

According to the Auditor-General, ECG failed to remit approximately GH¢1.4 billion in taxes, representing nearly half of the total unpaid tax obligations identified among the ten institutions.

The Ghana Airports Company Limited recorded the second largest outstanding tax obligation at about GH¢430 million, followed by the Produce Buying Company Limited with approximately GH¢330 million.

Other institutions cited in the report include GIHOC Distilleries Company Limited, Tema Oil Refinery, AirtelTigo Ghana and Graphic Communications Limited.

While the unpaid taxes dominated the report, the Auditor-General also identified irregularities across several other categories.

Cash irregularities amounted to approximately GH¢410 million, while loan irregularities stood at GH¢29 million.

Payroll irregularities totalled about GH¢19 million, procurement irregularities reached GH¢1.1 million, contract irregularities amounted to approximately GH¢3.3 million, while rent irregularities stood at about GH¢44,000.

Collectively, however, these categories represented only a small fraction of the overall irregularities compared with the scale of the outstanding tax obligations.

The findings suggest that the principal driver of the sharp increase in irregularities was not widespread growth in procurement or payroll breaches, but the accumulation of unpaid taxes by state owned enterprises.

That is particularly significant given government's continued emphasis on strengthening domestic revenue mobilisation and improving tax compliance across the public sector.

The report therefore raises questions about tax compliance within state institutions themselves, particularly as government continues to pursue broader revenue mobilisation reforms across the economy.

In recent years, authorities have introduced several tax administration measures aimed at improving compliance among private businesses and individuals. The Auditor-General's latest findings suggest that significant compliance challenges also persist within parts of the public sector itself.

Latest Stories

-

Pastors have more power to influence voters than politicians – Kumchacha

11 seconds -

Laryea Kingston issues come-and-get-me plea to GFA over Black Stars coaching role

29 seconds -

Some MMDAs take upfront payment for building permit instead of processing fees – Physical Planners claims

1 minute -

Two killed, two injured after police operation turns violent in Sefwi Sayerano

1 minute -

Alajo residents seek compensation ahead of planned demolition of waterways structures

3 minutes -

Police warn against unauthorised use of sirens, horns and strobe lights

4 minutes -

87 journalists trained on child trafficking reporting through IJM-GJA collaboration

5 minutes -

Ramaphosa’s proposed visit predates recent xenophobic attacks in South Africa – Kwakye Ofosu

9 minutes -

Nana Ama Bonsu assumes stool name Nana Yaa Akyaa II after enstoolment as Asantehemaa

18 minutes -

Accra floods: Task force identifies structures obstructing natural water channels at Oyarifa

19 minutes -

Accra floods: Flood Mitigation Task Force identifies encroachment at Tesa Dam near East Legon

20 minutes -

Political, traditional interference fueling Illegal developments – Physical Planners Association President

31 minutes -

About 1,300 applicants in recent security recruitment tested positive for HIV — Muntaka

37 minutes -

Muntaka announces new narcotics scanners for Ghana airports, ports and borders

43 minutes -

NACOC operates in only 66 districts due to resource constraints — Interior Minister

54 minutes