Audio By Carbonatix

When a central bank cuts interest rates while simultaneously spending billions to withdraw liquidity from the system, it is reasonable to ask: are these policies pulling in opposite directions?

This question arises from a deeper curiosity about how monetary policy is currently being conducted in Ghana. Over the past several months, the Bank of Ghana has been engaged in what appears to be a deliberate pattern: gradually reducing the policy rate while intensifying efforts to withdraw excess liquidity from the financial system.

The most recent decision to lower the policy rate from 15.5 per cent to 14 per cent simply brings this pattern into sharper focus. It is not an isolated move but part of an ongoing cycle of interest rate easing alongside continued sterilisation. At the same time, the scale of liquidity management has been substantial. The Governor recently disclosed that the Bank incurred about GH₵17 billion in 2025 in absorbing excess liquidity from the system.

At first glance, the combination seems puzzling. Lower interest rates are often associated with injecting liquidity. Sterilisation removes liquidity—at a cost. Why do both at once?

The answer lies in recognising that monetary policy operates through multiple channels, each targeting a different objective.

The Evidence: Easing Rates, Tightening Liquidity

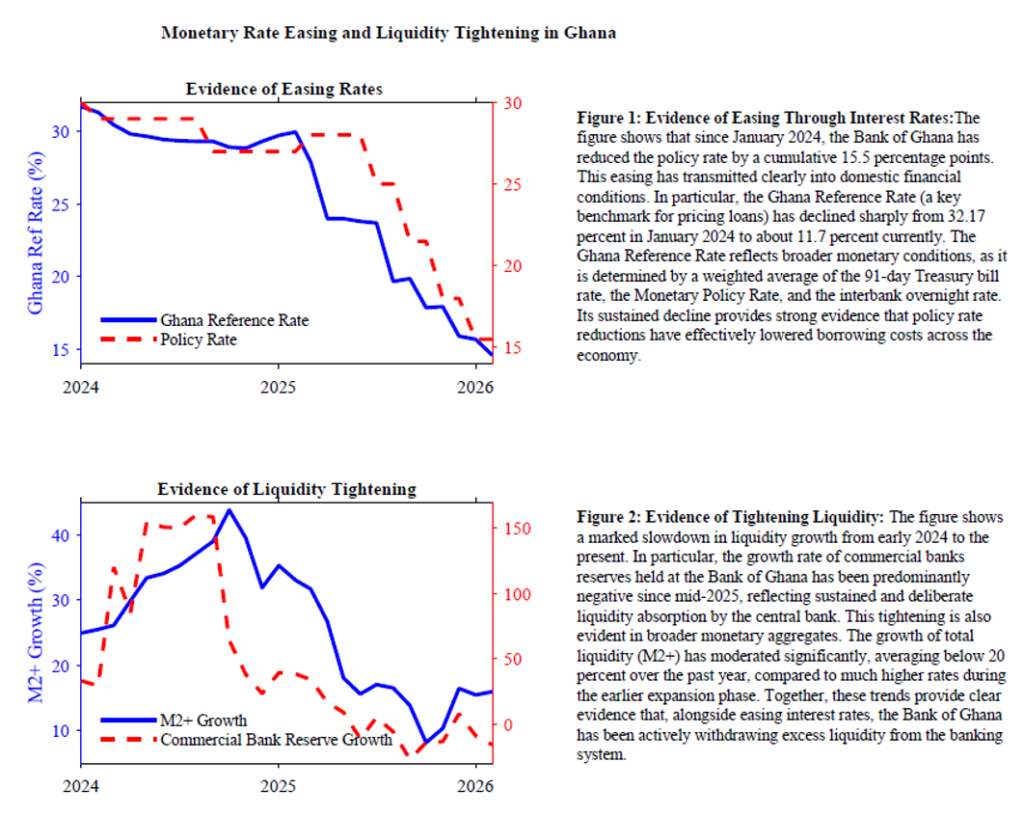

The data present a clear and consistent picture. On the one hand, interest rates across the economy have declined sharply. The interbank rate has fallen from above 27 per cent in early 2025 to about 12.6 per cent by February 2026, closely tracking the downward path of the policy rate (As shown in Figure 1). Treasury bill yields and lending rates have followed a similar trend. The sharp decline in the Ghana Reference Rate—from 32.17 per cent in January 2024 to about 11.7 per cent—further confirms that these policy rate reductions have been transmitted effectively into domestic financial conditions. This provides strong evidence that monetary easing is taking place through the interest rate channel, lowering the cost of credit across the economy.

At the same time, liquidity indicators tell a different but equally important story. As illustrated in Figure 2, system-wide liquidity has been tightening. Commercial banks’ reserves held at the Bank of Ghana—a key measure of available liquidity—have declined significantly, from over 74 billion cedis earlier in 2025 to about 60.8 billion cedis by February 2026. Moreover, the growth rate of these reserves has been predominantly negative since mid-2025, indicating sustained liquidity absorption. This pattern is reinforced by broader monetary aggregates. Growth in total liquidity (M2+) has moderated markedly, averaging below 20 per cent over the past year, a clear slowdown from earlier expansion.

Taken together, the evidence shows two developments occurring simultaneously:

- Interest rates are falling, easing financial conditions

- Liquidity is being withdrawn, tightening system-wide cash balances

Two Channels, Two Objectives

These developments are not contradictory. They reflect monetary policy operating through two distinct channels simultaneously.

The Interest Rate Channel: Supporting Domestic Recovery

The policy rate governs the cost of borrowing. With inflation now down to about 3.3 per cent, the need for very high interest rates has diminished. Keeping rates elevated would unnecessarily constrain credit, investment, and growth. The recent rate cut is therefore aimed at:

- easing financing conditions

- supporting private sector activity

- sustaining economic recovery

The Liquidity and Exchange Rate Channel: Preserving Stability

At the same time, the Bank is managing a large overhang of excess liquidity accumulated during the crisis period of 2022–2023. In Ghana’s context, this is critical because liquidity and exchange rate dynamics are closely linked. Excess cedi liquidity does not remain idle. It often flows into the foreign exchange market, increasing demand for dollars and putting pressure on the exchange rate. Exchange rate instability, in turn, feeds back into inflation. Sterilisation operations address this risk by:

- absorbing surplus reserves

- limiting speculative demand for foreign exchange

- strengthening the stability of the cedi

Why Not Do Neither?

This is the most important question. If lowering rates is associated with liquidity injection and sterilisation withdraws liquidity, why not do neither—and avoid the cost altogether? This is because the two actions are not substitutes. They do not cancel out. They operate on different margins of the economy.

- The policy rate determines the price of short-term funds

- Sterilisation determines how liquidity is allocated and used, especially in sensitive markets like foreign exchange

The liquidity associated with a rate cut is typically targeted and limited, aimed at guiding short-term interest rates downward. The liquidity being withdrawn, however, is structural and much larger, accumulated during the crisis period. If the Bank were to do neither:

- Borrowing costs would remain unnecessarily high

- Excess liquidity would continue to circulate

- Exchange rate pressures could re-emerge

- Monetary policy transmission would remain weak

In effect, the economy would face tight credit conditions alongside renewed financial instability.

A Lesson from the United States

A useful comparison comes from the United States, where recent monetary policy illustrates how these dynamics can coexist. Over the past year, as inflation eased, the U.S. Federal Reserve began cutting its policy rate. Starting in September 2024, when the policy rate stood at 5.25 per cent, the Fed reduced rates by a cumulative 175 basis points to about 3.5 per cent by December 2025. At the same time, however, the Fed continued its quantitative tightening (QT) program—systematically reducing its holdings of government securities and other assets. This led to a decline in the Fed’s balance sheet from approximately US$7.1 trillion to US$6.5 trillion, representing about an 8 per cent contraction. This reduction is particularly striking when viewed against the earlier expansion: the Fed’s balance sheet had surged from about US$4.2 trillion in February 2020 to US$8.9 trillion by June 2022 in response to the COVID-19 crisis.

The data, therefore, shows two movements occurring simultaneously:

- policy rates are declining, and

- Central bank assets are shrinking.

This was not interpreted as a contradiction. Rather, it reflected two distinct policy tools operating in parallel:

- Rate cuts to ease short-term borrowing conditions

- Quantitative tightening to withdraw excess liquidity accumulated during earlier stimulus

In essence, the Fed was lowering the price of money while normalising the quantity of liquidity. The Bank of Ghana is now operating under a similar logic—adapted to Ghana’s own economic realities.

A Deliberate Policy Mix

What may appear contradictory is, in fact, careful policy calibration.

The Bank of Ghana is:

- lowering interest rates to support recovery

- Withdrawing excess liquidity to protect the exchange rate

- Reinforcing macroeconomic stability

This is not an inconsistency. It is coordination

Conclusion: Not a Contradiction, but a Balancing Act

The Bank of Ghana is not working at cross purposes. It is navigating a complex transition—from stabilisation to recovery—using multiple instruments at once. Lowering the policy rate supports growth by easing credit conditions. Withdrawing excess liquidity safeguards stability by limiting pressures on the exchange rate. These actions may move in opposite directions on the surface, but they are aligned at a deeper level: both are aimed at sustaining macroeconomic stability while supporting a gradual recovery. The real challenge for monetary policy today is not choosing between easing and tightening. It is knowing where to ease, where to restrain, and how to do both without undermining either objective. And in that respect, the Bank of Ghana’s current approach is not a contradiction—it is a balancing act.

*******

Dennis Nsafoah is an Assistant Professor of Economics at Niagara University, NY and Member of Research Committee, Tesah Capital

Latest Stories

-

TVET workers lay down tools as union declares nationwide strike over unresolved concerns

30 minutes -

Black Stars begin Austria friendly preparation with 21 players

33 minutes -

Today’s Front pages: Tuesday, March 24, 2026

58 minutes -

Ghanaian citizen drags Attorney-General to Supreme Court over Kotoka Airport renaming

1 hour -

GACC unveils 25th anniversary logo to mark silver jubilee

1 hour -

Cutting rates while draining liquidity: Is the BoG contradicting itself, or getting it right?

2 hours -

Pepsodent “Smile Ride” brings oral health education to the streets of Ghana

2 hours -

Burkina Faso tomato ban exposes Ghana’s dangerous food dependency

2 hours -

Produce tomatoes in 90 days or step aside – FABAG fires warning at Agric Ministry

2 hours -

Mahama tours Nobi Agriculture Project in Afram Plains

2 hours -

Helicopter crash: Bawumia sends delegation to commiserate with founder of Hebron Prayer Camp

2 hours -

DVLA to establish office in Ketu North to boost service delivery – CEO

3 hours -

US bans new foreign-made consumer internet routers

3 hours -

Ho Central MP Richmond Kpotosu cautions drivers against overspeeding, drink driving

3 hours -

Ghana, Colombia seal maritime deal linking Tema and Cartagena ports

3 hours