Audio By Carbonatix

The Government of Ghana would require between US$600.0 million and US$800.0 million for external debt service in 2024.

Out of this, an estimated US$477.0 million would be used for Eurobond debt service.

According to IC Africa Research, the estimated cash flow on the restructured Eurobonds envisages the resumption of debt service on the restructured Eurobonds from July 2024.

“Accounting for the ongoing multilateral debt service (given that these debts were outside the perimeter of debt restructuring), we think the authorities would require between US$600.0 million – US$800.0 million for external debt service in 2024. These estimates exclude the US$1.6 billionn legacy arrears owed to the Independent Power Producers, out of which only US$400.0 million has been paid, and other commercial creditors”.

“Extending the outlook, the cash flow forecast shows intensified debt service obligation from 2026 – 2030, from peak US$1.4bn to US$1.1 billion on the Eurobonds alone”, it added.

However, Ghana’s forex reserves (excluding oil funds and encumbered assets) stood at US$4.3 billion in April 2024 (2.0 months of import).

This, IC Africa Research said emphasises its longstanding view that the government have been in reserves accumulation mode in anticipation of external debt service resumption rather than sufficient foreign exchange market support.

Consequently, it stressed that it remained less bullish on the outlook for the Ghanaian cedi as it sees limited sources of sizable foreign exchange (FX) inflow to the market.

Limited upside risks for secondary market pricing

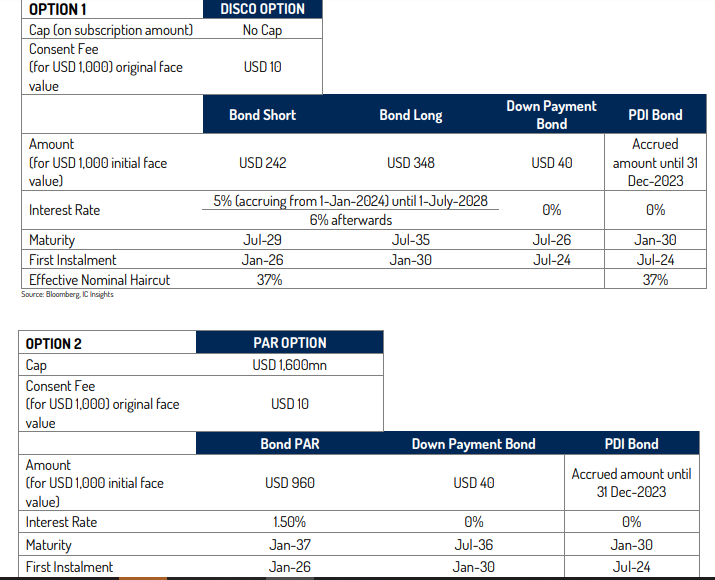

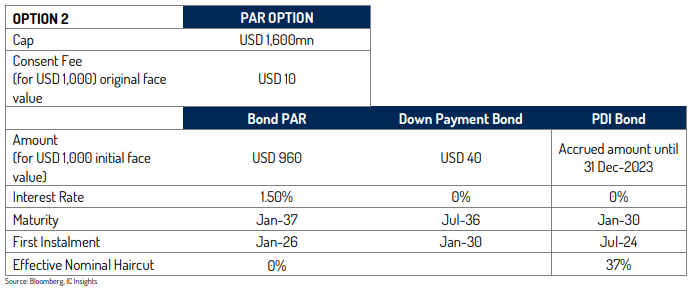

Following the significant move in restructuring the Eurobonds, IC Africa Research added that it envisages limited upside for secondary market pricing due to the deeper haircut and slashed coupon.

“Following our early May 2024 update note on the initial proposal in which we anticipated upside of between 10.0% and 20.0%, Ghanaian Eurobonds have posted an average price gain of 3.8% as of mid-day 24 June 2024. However, we opine that the new terms impose deeper losses on investors via the effective haircuts on principal and PDI, as well as the 50 basis points reduction in the stepped-up coupon rate (6.0%) while the lower coupon of 5.0% is extended for one extra year.”

“In view of this, we now see limited upside scope from the current average market cash price of US$53.4 per US$100.0 face value, with upside potential of between 5.0% – 7.0%.

Latest Stories

-

Chief Justice: Efficient Judiciary essential to reducing business costs

34 seconds -

Bayern grabs 99th-minute winner to cap superb fightback

37 seconds -

Ahmed Ibrahim urges Ghanaians to reflect Easter values in nation-building

4 minutes -

ECG inefficiencies undermining power supply -Mahama outlines reforms

6 minutes -

Lewandowski scores as Barca fight back to defeat Atletico

7 minutes -

Lack of private sector consultation undermining economic growth – Jerry Ahmed Shaib

11 minutes -

Real Madrid seven points adrift after Muriqi’s late Mallorca winner

11 minutes -

Ghana must lead AfCFTA implementation by example – Trade Minister Ofosu-Adjare

16 minutes -

Strong Judiciary key to business confidence – Chief Justice Baffoe-Bonnie

20 minutes -

Mahama announces 60-Hectare irrigation project to boost tomato production

27 minutes -

WPL: Hasaacas Ladies win on last day to set up final with Ampem Darkoa

27 minutes -

Chisora beaten by Wilder in captivating bout

51 minutes -

One dead, six maimed as bloody land feud tears Krachi Nchumuru apart

1 hour -

Missing service member rescued by US forces after jet downed in Iran, Trump announces

2 hours -

Gomoa Easter Carnival: Sarkodie, Kuami Eugene, Tinny, set festival ablaze as Day 3 ends on high note

2 hours