Audio By Carbonatix

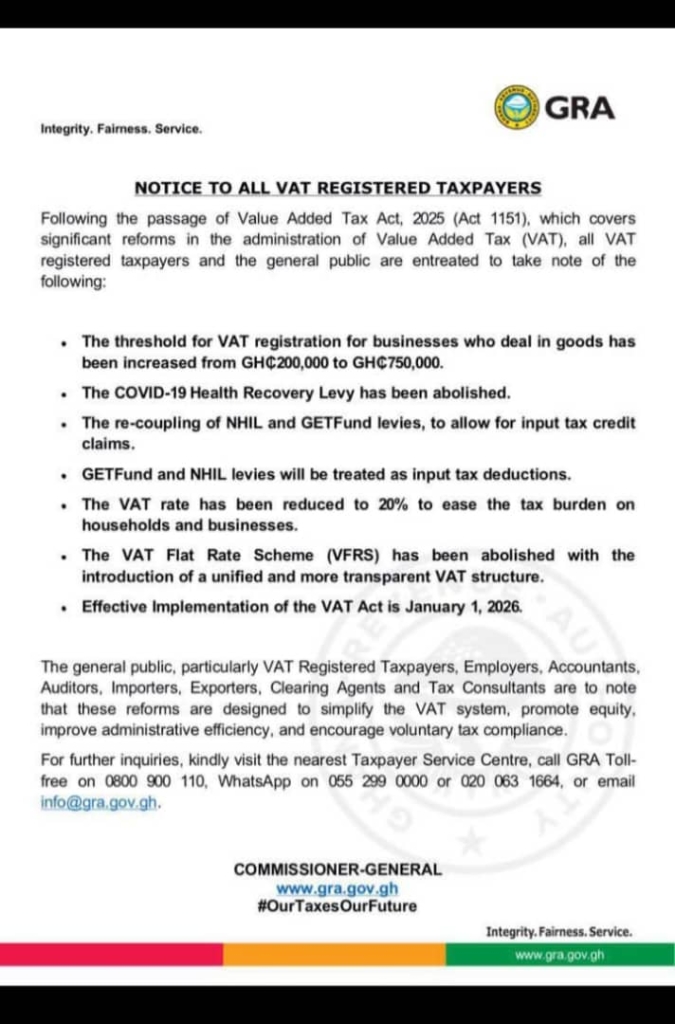

The Ghana Revenue Authority (GRA) has announced sweeping changes to the country’s Value Added Tax (VAT) regime following the passage of the Value Added Tax Act, 2025 (Act 1151), with the reforms set to take effect from January 1, 2026.

In a notice addressed to all VAT-registered taxpayers, the GRA stated that the new law introduces significant reforms aimed at simplifying VAT administration, enhancing compliance, and alleviating the tax burden on households and businesses.

One of the major changes is an increase in the VAT registration threshold for businesses dealing in goods. The threshold has been raised from GH¢200,000 to GH¢750,000, a move expected to reduce the number of small businesses required to register for VAT.

The Authority also announced the abolition of the COVID-19 Health Recovery Levy, which was introduced during the pandemic to support the government's expenditure.

Under the new VAT structure, the National Health Insurance Levy (NHIL) and the Ghana Education Trust Fund (GETFund) levies have been re-coupled, allowing businesses to claim input tax credits. Both levies will now be treated as input tax deductions.

In addition, the VAT rate has been reduced to 20 per cent, a measure the GRA says is intended to ease the tax burden on consumers and businesses.

The VAT Flat Rate Scheme (VFRS) has also been abolished, paving the way for a unified and more transparent VAT system.

The GRA explained that the reforms are designed to promote equity, improve administrative efficiency, and encourage voluntary tax compliance.

It urged VAT-registered taxpayers, employers, accountants, auditors, importers, exporters, clearing agents, and tax consultants to take note of the changes ahead of the implementation date.

The Authority further encouraged the public to seek clarification where necessary by visiting the nearest Taxpayer Service Centre or contacting the GRA through its toll-free line or official communication channels.

Read the full statement below

Latest Stories

-

GPL 2025/26: Dreams FC stage stunning comeback to hammer Eleven Wonders

1 hour -

Livestream: The Probe examines Kumasi’s looming water crisis

1 hour -

MTN Ghana gears up to lead Africa’s AI revolution

1 hour -

Philanthropist Alhaji FuZak donates Da’wah bus to Ambariya Sunni community

1 hour -

GUTA calls for suspension of Publican AI system over trade disruptions

1 hour -

TTAG raises alarm over proposed recruitment of 7,000 teachers, demands national posting roadmap

2 hours -

Civilians feared killed after reports of air strike on Nigerian market

2 hours -

Bishop Simon Kofi Appiah installed as new Jasikan Diocese Bishop

2 hours -

Trump’s Strait of Hormuz blockade threat raises risks and leaves predicaments unchanged

2 hours -

US Court backs extradition of former MASLOC CEO Sedina Tamakloe-Attionu to Ghana

3 hours -

Seven arrested as NAIMOS dismantles illegal mining camp, seizes firearms at Boin River

3 hours -

Fire erupts at Madina Ritz Junction, destroys multiple wooden structures and containers

3 hours -

Daniel-Kofi Kyereh returns from long-term injury, registers assist for Freiburg U23

3 hours -

Knifeman calling himself ‘Lucifer’ slashes three at NYC’s Grand Central

3 hours -

Brands are built from within to without

3 hours