News Prime | Power Outages: The Energy ...

AI in journalism: We will not ...

Cecilia Dapaah’s case: EOCO hasn’...

Power outages: We are not in ...

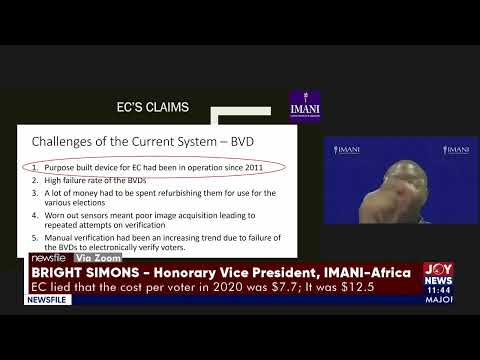

EC discards 10 BVDs: EC lied that ...

EC discards 10 BVDs: We should not ...

ECG cannot guarantee consistent power supply ...

Cecilia Dapaah’s case: What’s ...