Audio By Carbonatix

It seems the Bank of Ghana (BOG) May 2020 Monetary Policy Committee (MPC) Report cites the US Fed and US Treasury to prepare our minds for a significant shift in its past conservative fiscal stance to an aggressive one.

COVID-19 is a dangerous health and economic hazard but the change in BOG’s fiscal stance is stunning, given its record in recent economic crisis.

The Statement includes some bold assertions in Paragraphs 13 to 15:

“Preliminary assessments show that the financing gap that was estimated at the time of applying for the IMF RCF in March (2020) has widened significantly, resulting in a large residual financing gap”.

IMF’s RCF Report shows the COVID-19 fiscal gap as part of a widening 2020 Budget gap. The Minister went to Parliament in March and May 2020 on COVID-19 but did not present a Supplementary Budget to differentiate the two gaps. Nonetheless, the Statement is clear:

“Current market conditions in the wake of the pandemic, will not allow the financing of the gap from domestic debt capital markets without significantly increasing interest rates”.

BOG’s justification is a difficult domestic debt capital market conditions and a significant increase in interest rates. This is curious and difficult to justify since, as shown in Table 1 later, GOG’s borrowing from the World Bank, IMF, and other sources and its Stabilization Fund draw-down fully cover the extra COVID-19 expenditures.

“Under the circumstances and in line with Section 30 of the BOG Act, 2002 (Act 612), as amended, the BOG has triggered the emergency financing provisions, which permits the Bank to increase the limit of BOG’s purchases of government securities in the event of any emergency to help finance the residual financing gap”.

The fact that BOG had to invoke its 2nd level emergency powers to support the Budgetimplies that MOF has used its 1st level liquidity access to5 percent of prior year’s tax revenues (note: the Minister asked Parliament to raise to 10 percent).

“Today, under the BOG’s Asset Purchase Programme (APP), the Bank has purchased a GOG COVID-19 relief bond with a face value of Ghc5.5 billion at the Monetary Policy Rate with a 10-year tenor and a moratorium of two (2) years (principal and interest). The Bank stands ready to continue with its APP up to Ghc10 billion in line with the current estimates of the financing gap from the COVID-19 pandemic.

Without a House approval of a Supplementary Budget and “terms and conditions”, BOG has already purchased “COVID-19 Relief Bonds”.Given its name, the new GOG bond gives direct access to “budget” cash, compared with buying existing bonds. Traditionally, central banks buy existing market instruments during a financial crisis because it has a wider impact on more holders such as banks and finance houses. On a wider note, the action raises questions on the authority to declare “emergencies”, even if financial: Parliament, Cabinet, MOF or BOG.

- Overall versus COVID-19 fiscal gap

BOG’sreversal of a conservative fiscal stance through 2nd level emergency powers seems unprecedented but does not differentiate between the 2020 Budget and COVID-19 fiscal gaps. The Minister informed Parliament that the COVID-19 gap was Ghc9.5 billion, which can meet from its core COVID-19 inflows, as part of seems to be the approximatelyGhc50 billion overall fiscal gap to whichBOG appears to show commitment.

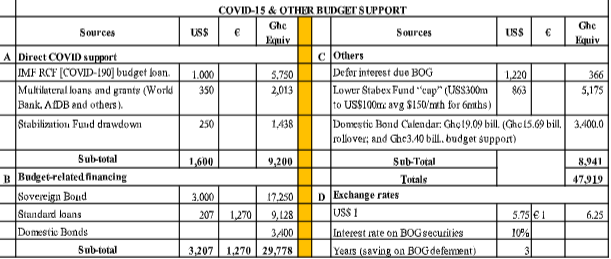

Table 1 shows (a) the COVID-19 Ghc9.51 billion inflows; plus (b)2020 Budget deficit of Ghc18.88 billion approved by Parliament; which (c) adds up to Ghc28.49 billion; being (d) far below the Ghc48.01 billion overall gap and total anticipated inflows.

Table 1: COVID-19 and other Budget support

The question is if a major fiscal correction is underway to align GOG’s unorthodox fiscal accounting with that of the IMF and others on the “parallel” reporting saga. The total funding of gap of US$47.92 billion less Ghc28.49 billion of budget deficit [Ghc 18.88 billion] plus COVID-19 gap [Ghc9.51 billion]—which implies that the non-COVID correction of Ghc19.43 billion exceeds the official 2020 Budget deficit of Ghc18.888 billion.

In his May 2020 Statement to Parliament, the Minister asked the House to approve a “recalibration”of the 2020 Budget to increase the overall fiscal deficit from Ghc18.9 billion (4.7 percent of GDP) to Ghc30.2 billion (7.8 percent of revised GDP).

This level of correction will be consistent with the Fund’s differentiation of RCF (COVID-19) and overall fiscal gap as well as inclusion of bailout and energy sector costs above the line—which MOF must show explicitly in the Supplementary Budget, not hidden in budget footnotes and appendices.

The “recalibration” of 2020 Budget deficitmeans an adjustment oftax and non-tax revenues, expenditures, arrears, and financing—a part of the Appropriation process under the Constitution PFMA.Parliament has approved the 2020 Budgetalready, hence the Minister must seek a Houseapproval in a Supplementary Budget. It seems a lot of financing has started before the PFMA’s deadline of end-July for a 2020 Supplementary Budget orCertificate of Urgency.

- BOG’ssupport and commitment

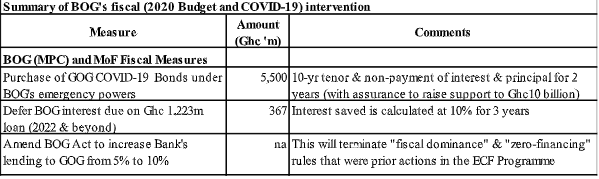

Table 2 shows that the immediate BOG fiscal support of Ghc5.877 billion is31 percent of the fiscal balance of Ghc18.888 billion in the 2020 Budget, which increases to 53 percent with escalation BOG support to Ghc10 billion. Given (a) absence of Supplementary Budget; and (b) RCF, other loans, and Stabilization Fund drawdown that appear to cover the COVID-19 needs, BOG seems to take major decisions on fiscal management that belong to only Parliament. These include the Appropriation of Public Funds (including BOG funds, as delegated by its Act) that the Constitution (and PFMA) reserves for House under the Constitution and PFMA.

Table 2: BOG’s 2020 Budget and COVID-19 fiscal gap measures

Conclusion

The difference between “COVID-19” and “overall 2020 Budget” fiscal gaps is a source of concern for observers of Ghana’s fiscal scene. One GOG reputation is its accelerated and significant fiscal consolidation under an IMF ECF Program from 2017 to 2019.

However, come time to draw on these savings, they seem to fizzle quickly and send GOG scrambling for loans and debt forgiveness, early in declaring COVID-19 a pandemic.

The IMF’s backdates to revise fiscal balances and public debt figures in the Article IV (December 2019) and RCF (COVID-19) Board Reports became controversial, as “parallel” and non-transparent to a section of Ghanaians. Nonetheless, they have helped with a better view of the fiscal situation.

This article highlights the central bank’s apparent role in the fiscal correction (with COVID-19 in the forefront), with the next one giving reasons for why we may be seeing a conservative stance change into an aggressive one.

The writer Seth E. Terkper is a former Finance Minister of Ghana.

Latest Stories

-

Transparency International calls for stronger reforms after survey reveals increased public bribery demands

7 minutes -

‘We miss his wisdom and guidance’ – Muniru Limuna’s son pays tribute at memorial service

9 minutes -

‘No speech can erase your pain’ – Mahama consoles families of helicopter crash victims

11 minutes -

Mahama urges recognition of public servants’ sacrifices as Ghana marks one year since helicopter crash

14 minutes -

Mahama urges Ghanaians to preserve legacy of ‘Departed 8’ through service and patriotism

23 minutes -

‘Finish their work’ – Samuel Aboagye’s widow urges action against galamsey to honour Departed 8

26 minutes -

Daily Insight for CEOs: Encouraging strategic experimentation

27 minutes -

‘They had dreams they hoped to fulfil’ – Mahama remembers Departed 8

27 minutes -

Oyoko Methodist SHS qualifies for 2026 NSMQ National championship after dominant regional showdown

28 minutes -

‘Memory is an obligation of every grateful nation’ – Mahama pays tribute to helicopter crash victims

34 minutes -

‘They never expected it would be their final journey’ – Mahama honours helicopter crash victims

35 minutes -

Jubed releases two new singles: ‘Garden’ and ‘Fall’

40 minutes -

‘We had to share gloves and boots’ – Ofori Asare reveals Black Bombers’ Commonwealth Games struggles

42 minutes -

Sarfo Duku commends Kotoko Board for ‘bold decision’ to sack four players

47 minutes -

‘Though a year has passed, it feels like yesterday’ – Family mourns Squadron Leader Anala

1 hour