Audio By Carbonatix

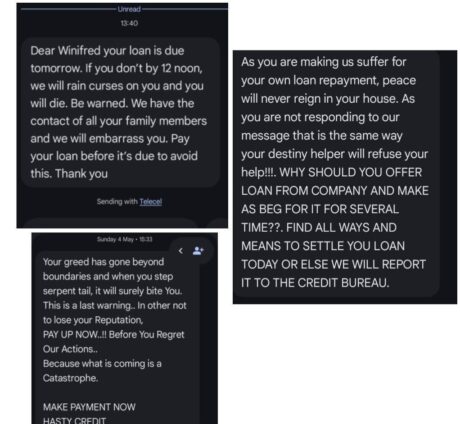

At 1:40 pm, the message came in.

“If you don’t pay by 12 noon, we will rain curses on you, and you will die… We have the contact information of all your family members, and we will embarrass you.”

Minutes later, another followed, escalating in tone and urgency. Then another, warning of catastrophe, shame, and irreversible consequences.

These were not anonymous scam messages. They came from a loan app.

The messages were sent by digital lending applications installed on this reporter’s phone during an investigation into Ghana’s fast-growing and largely unregulated online lending ecosystem.

Within days of downloading the apps, and even before repayment deadlines had passed, at least three of them issued threats.

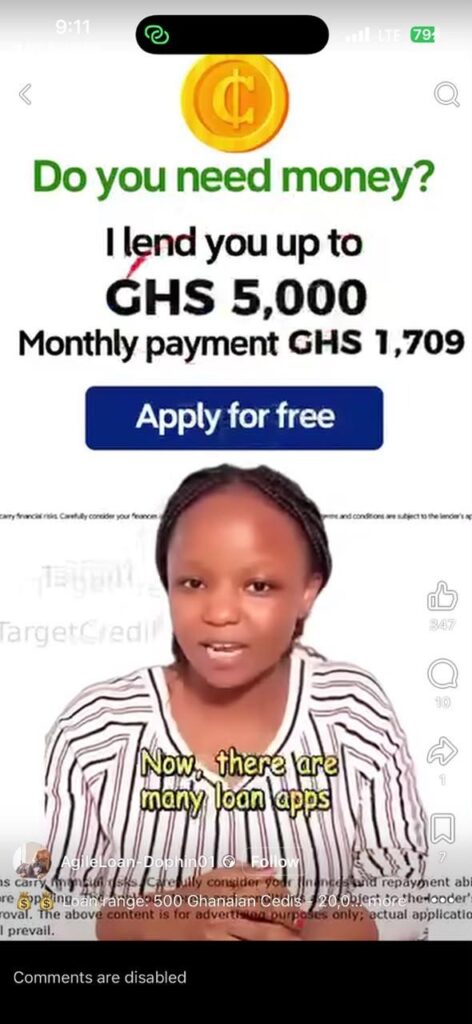

All of the apps had been encountered in the same way: through sponsored advertisements on platforms such as YouTube and Facebook.

The first encounter came casually, almost invisibly, while scrolling through Facebook late one evening.

Wedged between posts from friends and news updates was a sponsored advertisement promising “instant loans” of up to GHS5,000 with “no collateral” and approval in minutes. The ad featured bright colours, reassuring language and a prominent “Install Now” button.

Clicking through led directly to a download link. Within seconds, the application was installed. There were no obvious warning signs — no indication that the service was unlicensed or had been flagged by regulators. Instead, the interface mimicked that of legitimate financial platforms, requesting basic personal details before quickly escalating to demands for access to contacts, messages and location data.

What appeared to be a routine digital transaction was, in fact, the entry point into a system that would soon begin sending threats.

The investigation examines how unlicensed loan apps are using global advertising systems to reach vulnerable users in Ghana, despite being flagged by regulators.

Economic hardship fuels demand

For many Ghanaians, the entry point into this system begins with an emergency: a hospital bill, overdue rent, school fees, or a family crisis. Those moments increasingly collide with an economy where incomes struggle to keep pace with living costs.

Ghana's daily minimum wage stands at GHC21.77 (about $1.94), while the Ghana Statistical Service estimates that about one in four Ghanaians lives below the national poverty line, leaving millions with little or no financial cushion when unexpected expenses arise.

For many households, access to formal credit remains slow or out of reach, making the promise of an "instant loan" particularly attractive.

That is how 24-year-old Mary Ansah first came across TapLoan.

“I was at Lapaz Community Hospital with my mother,” she recalled. “I needed money urgently to pay for blood. The ad promised GHC500.”

Instead, she received GHC120. The repayment period was seven days, not the 30 days advertised.

What followed, she said, quickly spiralled beyond her control.

“They started calling me constantly — morning, afternoon, night,” she said. “Then the messages began. They said they would contact my family and disgrace me. And the interest rate was three times what they advertised.”

Within days, the threats intensified. Ansah said she began receiving messages warning that her contacts would be exposed and that she would be publicly shamed if she failed to repay on time.

“I couldn’t sleep,” she said. “Every time my phone rang, my heart would start racing. I was scared they would actually do it.”

The pressure forced her to turn to friends for help, borrowing money just to repay the loan and stop the harassment.

“I had to beg people I wasn’t even close to,” she said. “It was embarrassing.”

Even after repayment, she said the experience lingered.

“I deleted the app, but I was still anxious. I kept thinking they still had my information.”

“It almost destroyed me,” she added, referring not just to the debt, but the fear, humiliation and stress that followed.

Her experience mirrors that of Mohammed Abubakar, who downloaded Hasty Loan and Agile Loan while studying at the University of Ghana during a difficult financial period.

“The interest rates were unbelievable,” he said. “And they never said that in their advertisement.”

Across multiple applications tested in this investigation—including Agile Loan, Loan Base, Hasty Loan, Agil Credito, AgyapaCredit, Drive Lend, Cashpal, Sika Credit, BoseaFie Loan, Kudi Credit, TapLoan, EazyCash, and WiseLend, a consistent pattern emerged.

Loans were often disbursed below advertised amounts, repayment windows were extremely short, and interest rates escalated rapidly. What followed, however, was more troubling than the financial terms.

Before a loan is even approved, users are required to grant sweeping permissions to their devices. These include access to contacts, SMS messages, call logs, location data, and stored files. Without granting these permissions, the apps simply do not function.

Borrowers trapped in a cycle

Dr Arnold Kavaarpuo, Executive Director of Ghana’s Data Protection Commission, warned that such instant loan aps violate the law.

“Loan apps cannot threaten to use personal data for intimidation, that is illegal,” he said. “The principle of purpose limitation means data collected for one reason cannot be repurposed to harass or coerce users.”

He added that companies are required to register with the commission and collect only data that is strictly necessary, noting that once personal data is exposed, “it becomes very difficult to regain control over it.”

The scale of the problem is also visible in online communities where borrowers share their experiences. In one public Facebook group titled “Say No to Loan App,” which has more than 50,000 members, users describe cycles of debt, harassment and desperation.

“I’m having sleepless nights… overthinking can kill a person. I borrowed from one loan to pay another,” one anonymous member wrote. Others warn against falling deeper into debt, while some users—still in urgent need—post requests for new loans, even offering collateral.

The conversations reveal a troubling pattern: victims of predatory lending often remain trapped within the same ecosystem, oscillating between seeking help and being drawn back into it.

For many users, this step is taken without hesitation, driven by urgency rather than caution.

“When you’re desperate, you’re not thinking about permissions,” said Adobea Biritwum, a product manager and technology analyst. “You just need the money. But that’s exactly what they exploit.”

Once access is granted, the dynamic shifts. Borrowers report receiving threats that their contacts will be notified, their employers contacted, and their reputations damaged if payments are delayed. In some cases, victims say these threats are carried out.

An insider speaks

An employee who works with one of the apps, TapLoan, confirmed that these tactics are not incidental but part of a structured system. Speaking on condition of anonymity for fear of losing her job, she described a routine built around intimidation.

“Every week we have a schedule,” she said. “We call customers who are about to default — a day or two before their deadline — and threaten them. It’s a directive from our boss.”

She said staff are also required to escalate to verbal abuse once payments are missed.

“For those who have defaulted, we call to insult them. We run this shift every day, from threatening to insulting people. It’s exhausting.”

The employee said she had worked with the company for less than two months and took the job out of financial necessity.

“I’m an unemployed graduate, so I decided to stay a bit until I get a better job,” she added.

While the claims could not be independently verified, they align with testimonies from multiple borrowers interviewed.

The platform problem

In response to a Right to Information request, the Bank of Ghana confirmed that all the apps identified in this investigation are unlicensed and warned the public to avoid them. Yet despite this, they continue to reach users through paid advertising on global platforms.

During a three-week monitoring period, sponsored ads for at least six of these apps were observed across Facebook, Instagram and YouTube, often using near-identical language promising “instant loans” and “no collateral”. The investigation found that apps flagged as illegal locally are still able to scale through global advertising systems that operate beyond the reach of national regulators.

This contradiction, illegal under local regulation but promoted through global digital infrastructure, lies at the centre of the issue.

When contacted, Meta said it has strict policies governing financial advertisements and had removed ads associated with some of the identified pages for violating its rules. However, independent checks conducted during this investigation continued to identify similar ads running during the reporting period.

Google, meanwhile, states on its safety platform that keeping users safe online is its highest priority. However, the company did not respond to detailed questions about specific advertisements identified in this investigation.

Evidence gathered over weeks—including active advertisements, downloads and user experiences—suggests that enforcement remains inconsistent, particularly in markets like Ghana.

For Emmanuel Nii Foli Creppy, an AI governance consultant, the problem is not incidental but systemic.

“Global platforms cannot claim neutrality,” he said. “They accept advertiser payment, algorithmically target audiences, and profit from every impression served.”

At the heart of the issue is a disconnect between regulatory systems and platform infrastructure. The Bank of Ghana maintains a database of licensed financial institutions, while platforms operate their own advertiser verification systems. However, these systems do not communicate.

“No live regulatory interface exists,” Creppy explained. “When a lender is unlicensed, no automated signal reaches the ad platform.”

The result is a predictable gap in enforcement.

Users experiencing financial distress are more likely to click urgent loan advertisements. The system detects this behaviour and optimises accordingly, delivering more of the same content to similar users.

“The algorithm is a very fast, obedient machine trained to fetch money — clicks, installs, sign-ups,” Creppy said. “It does not know if what it is fetching is harming people.”

For many, however, the decision to click is not about ignorance, but necessity.

“People don’t have options,” Biritwum said. “If I need GHC500 urgently, I’m not going to stop and check whether an app is licensed.”

That gap between urgent need and institutional protection is precisely where these apps thrive.

For now, the consequences are borne by individuals.

A young woman trying to save her mother. A student navigating financial hardship. A phone lighting up with threats of death, shame and exposure.

All triggered by a click on a sponsored advertisement.

Until the systems that enable this are meaningfully addressed, through regulation, enforcement, and accountability, the ads will continue to run, and the messages will continue to come.

This article was published under the Tech Justice and Platform Accountability Project of the Centre for Journalism Innovation and Development (CJID), with support from Luminate.

Latest Stories

-

Samsung introduces 2 new products into Ghanaian market

9 minutes -

Spend to complete abandoned projects – Abena Osei-Asare tells government

22 minutes -

Daily Insight for CEOs: Expanding influence through partnerships

27 minutes -

US says it will use frozen Iranian assets to fund damage to ships as strikes continue

30 minutes -

Don’t just spend, invest in areas that transform lives — Abena Osei Asare tells government

32 minutes -

Police reject GH¢150,000 bribe after 5,000 parcels of suspected narcotics in Tema

33 minutes -

Should a good leader be feared or loved? A critical look at Ghana’s recent presidential leadership styles

33 minutes -

Sammy Gyamfi rejects Minority’s claims, insists GoldBod remains financially strong

34 minutes -

Nkoko Nkitinkiti is working despite isolated cases of beneficiaries eating chickens — Ato Forson

36 minutes -

128 students to leave Ghana for educational exchange across four European countries

46 minutes -

Finance minister clarifies agriculture ministry allocation dispute

48 minutes -

National Community Media Cyber Capability Building Project to launch on August 3

1 hour -

Two Chinese win world’s top Maths prize for solving century-old problems

1 hour -

Today’s Front Pages: Friday, July 24, 2026

1 hour -

France orders evacuation of tourist spot as hundreds flee wildfires by boat

1 hour