Audio By Carbonatix

From a serious policymaking point of view, the question as to whether “Ghana should go to the IMF” is not a complete, or particularly meaningful, one.

The IMF has many product lines, designed for different purposes, so the more appropriate questions are:

- Should Ghana go for a/some IMF product(s)/program(s)?

- If yes, which?

- What are the costs and benefits?

In actual fact, two of the key functions of the IMF result in some pretty automatic programs for all 190 countries in the world that have signed the Bretton Woods Agreement.

It helps to recall that as the second world war was drawing to a close, and the increasingly triumphant American-led bloc was designing how they were going to govern the world they were about to inherit, economic “viruses” like hyperinflation and shortage of goods, both in the earlier interwar period and during the war, had already shown clearly how contagious they could be if countries do not work to stem their spread. Just like COVID-19.

Even a casual look at the four main functions of the IMF immediately points out which two should be considered “baseline” for all participating countries:

- Surveillance of the international monetary system

- Monitoring of members’ economic and financial policies

- Provision of Fund resources to member countries in need

- Delivery of technical assistance and financial services.

All countries in good standing and in “continuing communion” with the IMF cooperate with it on the first two functions. That fact can be translated to mean that every one of the 190 countries have a program of some sort with the IMF. The famous Article IV “Consultations” that see the IMF hold bilateral discussions with member state governments almost every year is legally grounded in the surveillance and monitoring powers granted to the Fund under the 1944 Agreement.

So, presumably, when sensitivities emerge about whether Ghana should do business with the IMF, the issue is about the last two functions: borrowing money and/or being subjected to something akin to “technical supervision” of how the government of Ghana conducts its business of governing the economy. But even in respect of these two areas, as I have already stated above, the Fund is like a restaurant with a menu. There are varied dishes and a bit of room for some customization. Every program is designed on the back of a bespoke agreement. Much depends on a country’s negotiating skill.

It is a bit sad, for all the foregoing reasons, for the Finance Ministry to simply bundle everything IMF into the “bailout” category. By making the government’s IMF posture look like a patriotic avoidance of beggary and prostration before a foreign overlord, the Finance Ministry has completely distorted a proper discussion about “what Ghana can use the IMF for” strategically.

Such conduct follows in a line of worrying missteps in the ongoing management of Ghana’s revenue crisis. Sound analysis requires robust debate about all the options available to Ghana in these trying times. The “echo chamber” style of governance, often neglecting facts and data, is estranging the policy community in Accra, who no longer finds a counterpart in the government for genuinely robust policy engagement.

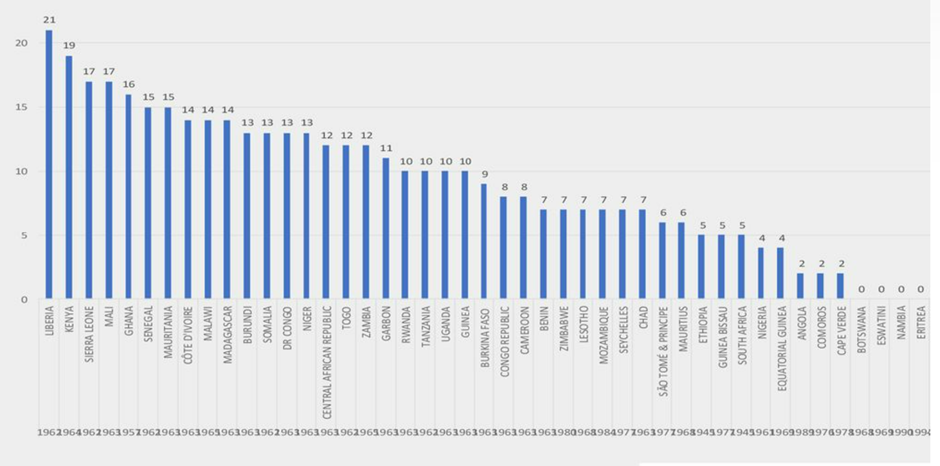

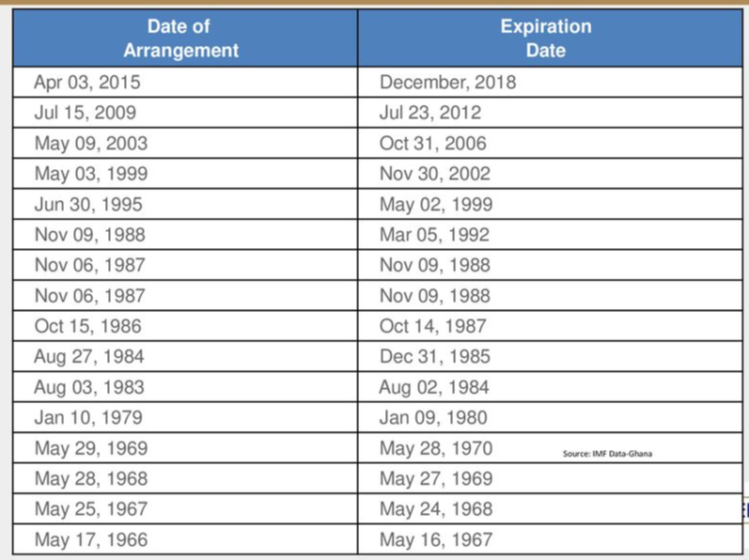

IMANI’s Professor Bopkin, something of a scholar of Ghana-IMF relations. He has helpfully produced the chart and table below to show that Ghana is the 5th most enthusiastic IMF customer in Africa. The country has approached the Fund 16 times since it joined in 1957. Since then, usually after every political transition or onset of major reforms, Ghana “goes” to the IMF.

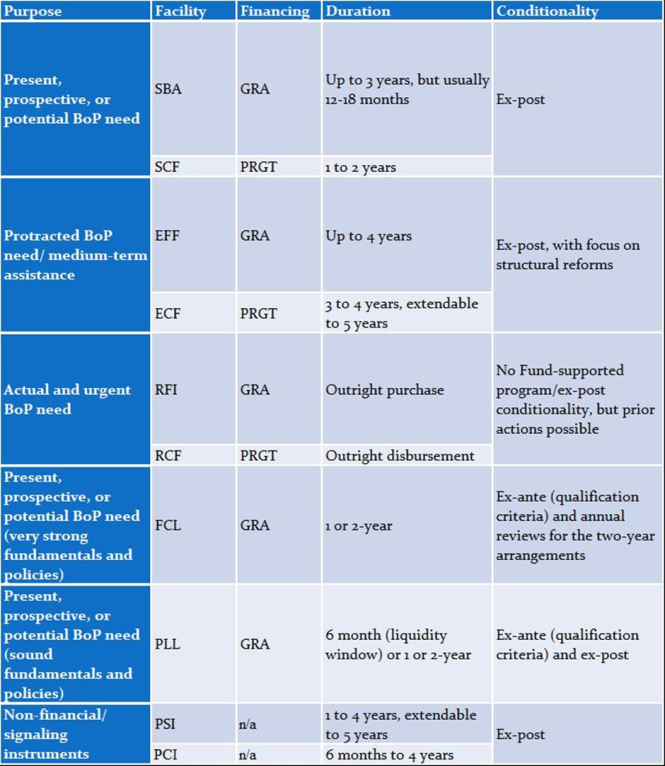

A deeper dive into the details shows that the aversion of some economic managers for IMF “conditionality” (terms or conditions associated with some of the IMF products) generally result from the type of products Ghana usually qualifies for. Ghana’s IMF engagements have often been characterised by long-term (3 to 5 years) and intrusive arrangements. But those are not the only offerings in the Fund’s stables.

Below is a quick overview of the most popular IMF products.

Ghana’s practice over the years has been to wait until it is almost desperate before approaching the IMF. It therefore finds quite often that it only qualifies for programs like the Enhanced Credit Facility (ECF) and Extended Fund Facility (EFF) that deserve some of their reputation for reducing political flexibility. IMF programs requiring “structural reforms” of the economy do certainly signal to the market that a country is in a bit of a patch, a factor that can, in certain circumstances, affect borrowing on the commercial market. But there is a lot of nuance.

Kenya, for instance, is actually consuming three IMF products concurrently, all of the “bailout” variety – the EFF, ECF and the RCF. Through these facilities, it has secured nearly $2.2 billion in the last two years alone (twice what the e-Levy is expected to yield in the Finance Ministry’s most optimistic forecasts).

Ghana decided in 2020, like Nigeria, to take advantage of a global COVID-19 response mechanism and go for just an RCF, which is a fairly sweet-deal kind of bailout package with virtually no conditions. It received 738 million SDR, a type of IMF “currency” or unit of account (or roughly $1 billion), whilst Nigeria, because of its bigger economy, bagged 2.45 billion SDR. In both cases, the “program” expired soon after the money hit the account. Behaving just like a normal commercial loan, where the bank generally leaves the borrower to run their business as they see fit.

The above suggests that Ghana has no problem taking IMF money per se. But, like Nigeria, its twin on quite a number of fiscal measures nowadays, it does not appreciate any schoolmaster type tutelage. Which is fine, but a number of strategic issues arise, almost none of which has been properly debated.

Why is the Finance Ministry not going for a Rapid Finance Instrument (RFI) product like Namibia (2020), Senegal (2020), Bahamas (2020), and Costa Rica (2020)? Surely, these are not basket-case countries? The RFI product is also light-touch, with virtually no conditionality. South Africa successfully negotiated a $4.3 billion RFI facility in July 2020. Once the money hit the account, that was it, just like a normal commercial loan. The IMF actually do call these “outright loans”, and packages them with no conditions other than the standard interest and repayment terms.

There is a very important reason why this is a crucial point. IMF money is cheap. Many of its products are interest rate free until the borrowing country exceeds 187.5% of its quota, at which point the rate hits 2%.

Some products like the RCF are not only interest free regardless of amount, they also come with a grace period, typically 5 years during which the country pays nothing.

Compare that with a tranche in Ghana’s most recent Eurobond issuance in 2021. A 7-year $1 billion bond that attracted interest of 7.75%. In very crude terms, Ghana “loses” $57.5 million a year by borrowing a billion dollars in the commercial markets instead of from the IMF. Not chicken feed.

So, if IMF money is cheap, why can there be any concern at all? Well, as you may recall from above, there is also the issue of “national ego” and the more pragmatic concern about “market signaling”. Let’s talk about the latter.

Some observers erroneously believe that an IMF program somehow blocks a country from borrowing on the international markets until the program is complete. This is of course completely inaccurate. Kenya successfully issued a $1 billion Eurobond in June 2021 at a fairly decent rate of 6.3% just two months after securing a $2.34 billion IMF facility. In some ways, getting an IMF facility can actually improve the market’s perception of a country’s creditworthiness. Ghana tested this in 2015 when after enrolling in an IMF program in April it approached the market in October of the same year with a Eurobond issuance. Being at the height of the dumsor crisis, it didn’t get a good rate, but at least it sold.

The signaling issue is thus not open and shut. And, of course, if Ghana believes that national pride prevents it from appearing as if it needs an IMF stamp to be able to access the international capital markets, why does it not try for the big leagues?

There are a number of IMF programs that only the “big boys” go for. They include the Flexible Credit Line (FCL) and the Precautionary and Liquidity Line (PLL). In November 2021, Mexico went for a $50 billion FCL. Chile had earlier collected nearly $24 billion in May 2020. Panama went for a $2.7 billion PLL in the same timeframe. If Ghana genuinely believes that its fundamentals are solid, as the Finance Ministry has said, and that it cannot be seen, in the remotest, to be experiencing a balance of payments situation, then why not test the country’s mettle by going for a PLL or FCL, both of which are only granted, like a revolving overdraft, to countries with sound economic fundamentals so long as they continue to meet the eligibility criteria? Unless, of course, things are not that rosy, and the Ministry is afraid that Ghana may not be eligible for anything other than plain-vanilla balance of payments support.

The last issue to consider is the “competition” between e-levy and an IMF program. Some commentators are promoting a “return” to the IMF as an alternative to going ahead with the e-Levy. This only makes sense if, as some suspect, the government’s intention of passing the e-levy is to convince the market to become more receptive to another Eurobond issuance. If that is indeed the case, then given the political costs of the e-Levy strategy, an IMF program would make more sense, especially when you reflect on the earlier point about how countries have often sequenced their Eurobond campaigns right after entering an IMF program.

If, on the other hand, the government is genuine in its rhetoric about cutting down borrowing, from whichever source, however cheap or well-priced, and getting Ghanaians to fund the greater part of their own government, regardless of the political and economic repercussions, then of course the e-Levy is a superior idea. After all, cheap as they may be, IMF facilities (except the relatively smaller “Catastrophe containment” grants) still need to be paid back.

Somehow, many in the policy community are not too convinced that the government’s recent actions are not merely a show for investors to reopen the doors to the sweet nirvana of Eurobond issuances. Early indications of the government’s domestic borrowing plans do not really corroborate the notion of significantly cutting its overall borrowing appetite.

Whatever be the fact, there is one certainty: neither an IMF program nor the e-Levy can truly address the fundamental issues that have led Ghana into the current ditch: weak productivity in the private sector exacerbated by a high cost of doing business, which in turn is compounded by wasteful spending habits in a fast-bloating state sector.

As I have argued elsewhere, the Ghanaian government has over the last decade become overbearingly expensive to run, with too many price-inflated projects competing for the attention of the politically connected. This has led to a neglect of quality policymaking that can actually boost efficient private sector output. Without the latter, GDP growth will not translate into jobs, innovation, and taxes.

In a way, talk about both e-Levy and IMF-return are distractions from the most critical issues at stake. Even if, depending on the real intentions of the government, one of the two is bound to be superior to the other.

Latest Stories

-

Muftawu Nabila’s report from New York as Ferran Torres extra time strike wins Spain World Cup title

11 minutes -

Mbappe first to win World Cup Golden Boot twice

28 minutes -

Spain battle past 10-man Argentina 1-0 in extra time to win World Cup

33 minutes -

New EU border system tripling time at passport control, airport boss says

51 minutes -

Shakira, Madonna, Justin Bieber and BTS perform at colourful World Cup half-time show

1 hour -

At least six dead and 21 injured after 2 earthquakes in Peru

2 hours -

Ferry carrying 133 passengers and crew sinks off Guyana coast

2 hours -

Publish Constitution Review Committee report before assenting to Tribunals Bill – Bawumia challenges Mahama

2 hours -

T-bills: Government exceeds target by 73%, interest rates decline

2 hours -

Sammi Awuku welcomes reconstitution of Ghana Tourism Authority Board after raising legal concerns

2 hours -

Photos: ECOWAS backs Ghana’s anti-xenophobia petition to AU

2 hours -

NPP ready to engage in consultations on Tribunals Bill – Bawumia

3 hours -

How to spot and avoid task scams on WhatsApp, Telegram

3 hours -

Ghana Electronic Procurement System will reduce corruption in public procurement – PPA

3 hours -

Ghana needs stronger courts, not a parallel justice structure – Bawumia on Tribunals Bill

4 hours