Audio By Carbonatix

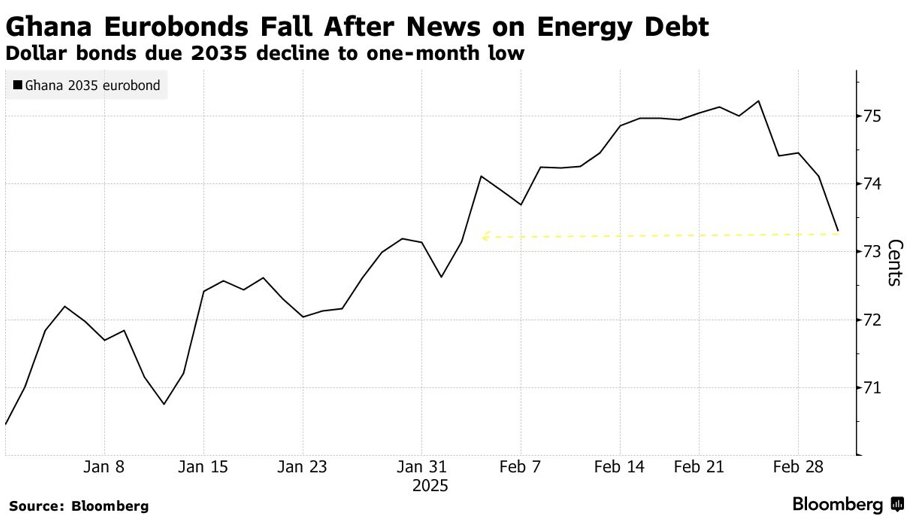

Ghana’s Eurobonds fell sharply on Tuesday, 4th March 2025 ranking among the worst-performing assets in emerging markets.

This followed Finance Minister Cassiel Ato Forson’s warning during the national economic dialogue in Accra, on Monday, 3rd March 2025 that the country’s energy sector debt could double to $9 billion by 2027 without urgent intervention.

When the cedi depreciates, Ghana’s debt burden increases, making repayments more expensive. Investor confidence in Ghana’s Eurobonds fluctuates based on economic stability, fiscal policies, and debt management strategies.

According to Bloomberg data, Ghana’s dollar bonds maturing in 2035 dropped by 1.1% to 73.3 cents on the dollar, reaching their lowest level in a month, while securities due in 2030 fell by 0.9% to 77.83 cents.

The Electricity Company of Ghana (ECG) has been a major contributor to the rising energy debt, Forson explained, as it can only account for 62% of the electricity it purchases due to distribution and collection inefficiencies. He also attributed the crisis to low electricity tariffs and lack of competition in power generation.

Despite restructuring most of its 737 billion cedis ($47.5 billion) public debt in October—including Eurobonds—Ghana remains in negotiations with 60 international banks to restructure $2.7 billion in loans. President Mahama has pledged to curb government spending, refine the IMF’s $3 billion programme, and rebuild investor confidence in Ghana.

Energy Minister John Abdulai Jinapor has indicated that the government will explore private sector participation in energy distribution and revenue collection. Within six months, a decision will be made on whether to pursue full privatisation or a concession model, where a private entity would manage operations for a fixed period before handing control back to the state.

Latest Stories

-

Ghana not out of the woods yet; economic numbers show more work is needed – Vice President of Chartered Institute of Taxation

25 minutes -

Modi’s education minister quits as jubilant Indian youth protesters claim victory

27 minutes -

OSP should not be solely blamed for Ofori-Atta situation – Prof Atua

2 hours -

US immigration judge had no jurisdiction to rule on Ofori-Atta’s criminal case – Inusah Fuseini

2 hours -

Final repatriation phase begins as another batch of Ghanaians is expected to leave South Africa

2 hours -

Atta Akyea urges patience in Ofori-Atta’s case, calls for voluntary return

2 hours -

Wontumi should not be made a sacrificial lamb to deter illegal mining – Atta Akyea

3 hours -

Wontumi to appeal conviction next week, seek bail pending appeal- Atta Akyea

3 hours -

Trump orders Smithsonian to post warnings about ‘inaccurate’ US history

3 hours -

Woman dies and child injured in collision between car and truck

3 hours -

Trump takes swipes at press during White House Correspondents’ Dinner

3 hours -

Atta Akyea says AG’s position supports Wontumi’s no-case submission argument

3 hours -

Ghana seeks stronger economic partnership with Egypt ahead of 70 years of diplomatic relations

3 hours -

Atta Akyea disputes judge’s conclusions on evidence in Wontumi illegal mining case

3 hours -

North East Regional Minister inspects development projects, warns conflict-prone communities

3 hours