Audio By Carbonatix

Asset management company, Tesah Capital, has described as bold and necessary for debt sustainability, government's plan to raise ¢100.5 billion in total revenue for the 2022 fiscal year.

Tesah Capital notes the projected revenue which represents a 42.9 percentage points increment (¢30.5 billion) on the 2021 revenue outturn of ¢70.34 billion will increase the revenue generation capacity of the country.

The projected revenue increment, the company believes, is necessary given that the country has long suffered from narrow revenue mobilisation due to the existence of a large informal sector.

“The country depends largely on indirect taxes and import income from few primary commodities; though direct taxes as a share of total taxes witnessed some improvement from 42 per cent in 2017 to 50 per cent in 2020. Revenue targets have been missed for most of the years, from 2017 to 2020, highlighting the weakness in revenue forecasting capacity,” Tesah Capital noted in its review of the 2022 budget.

The projected 42.9 per cent revenue increment is expected to be achieved by government through the introduction of the electronic transaction levy, the 15 per cent increment in government services, reintroduction of the 3 per cent Flat Levy, property rates and government’s new resolve to pass the tax exemptions bill in 2022 to check revenue leakages as the immediate steps to increase revenues.

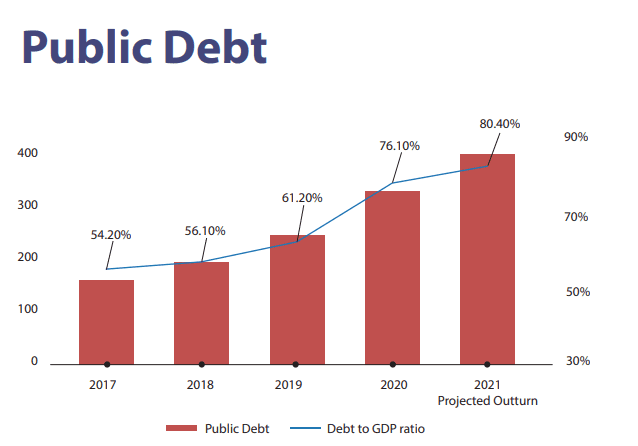

At the moment, Ghana's public debt is unsustainable and pegged at 77.8 per cent of Gross Domestic Product (GH₵341.8 billion) and is further projected to continue on an elevated path.

According to Tesah Capital, public debt as a ratio of GDP is expected to hit 80.4 percent by the end of 2021.

Of the total debt, domestic debt will amount to ¢185 billion representing 52.3 percent of GDP with external debt also amounting to ¢169 billion representing 47.7 percent of GDP.

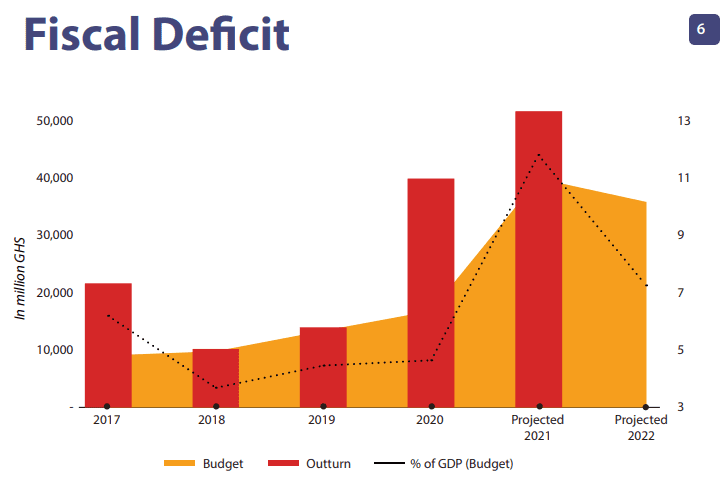

Tesah Capital adds that the projected 7.4 percent fiscal deficit (¢35.11 billion) for 2022 will increase the public debt to ¢395.81 billion.

"The expected fiscal deficit of cedis 35.11 billion cedis will increase the public debt to cedis ¢395.81 billion. The rising inflationary risk in advanced economies implies that the government will face an increased cost of financing the debt through international debt markets.

"This suggests that the government is likely to continue with the trend of using the domestic debt market to finance a larger portion of the public debt. Increased borrowing in the local debt market could lead to an increase in interest rates and crowd out the private sector from the loan market," the AMC notes.

Interest payments and employee compensation to decline

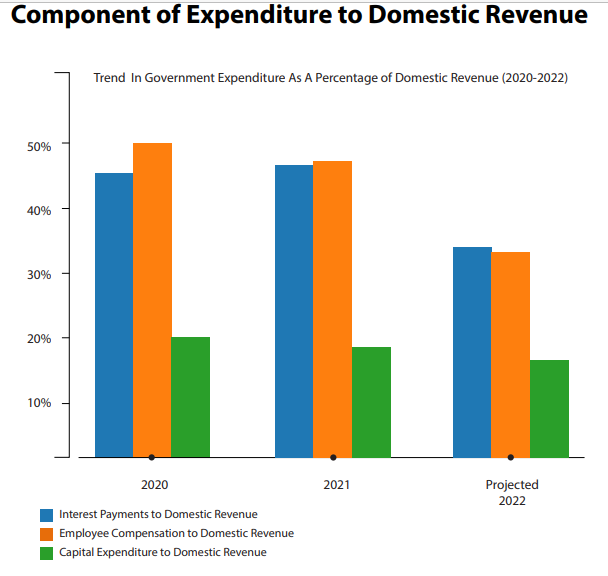

Interest payments, employee compensation and capital expenditure as components of domestic revenue Tesah Capital asserts are expected to marginally decline in 2022.

According to Tesah Capital, interest payments, employee compensation and capital expenditure over the last three years have been a major drainer of domestic revenue averaging 43 percent, 45 percent and 19 percent respectively.

"However, their component of domestic revenue is expected to decline from 47 percent, 48 percent and 18 percent in 2021 to 38 percent, 36 percent and 16 percent in 2022 respectively," Tesah Capital notes.

The marginal decline in the components of government's expenditure, Tesah Capital states, is as a result of the relatively higher projected growth in domestic revenue (30.5 percent) compared to projected growth in Interest payments (13.1 percent), employee compensation (7.9 percent) and capital expenditure (22.3 percent).

Projected total expenditure for the 2022 fiscal year (including payments for the clearance of arrears) is ¢137.5 billion, equivalent to 27.4 percent of GDP.

The expenditure estimate for the 2022 fiscal year represents a growth of 23.2 percent above the projected outturn of ¢111.6 billion, equivalent to 25.3 percent of GDP for 2021.

Key drivers of expenditure growth include capital expenditure, funding of key government flagship programmes, wage bill and interest payments.

Latest Stories

-

National Community Media Cyber Capability Building Project to launch on August 3

13 minutes -

Two Chinese win world’s top Maths prize for solving century-old problems

30 minutes -

Today’s Front Pages: Friday, July 24, 2026

32 minutes -

France orders evacuation of tourist spot as hundreds flee wildfires by boat

34 minutes -

25 Ghanaians claim asylum in Canada after World Cup 2026

43 minutes -

Youth unemployment now a national security threat — Economic Fighters League

47 minutes -

Mobilising resources for Ebola response: Africa CDC boss calls for more

1 hour -

2026 Mid-year budget: Growth without jobs not enough — Prof. Boadi warns

1 hour -

Enoch Amegbletor eyes Volta Regional NPP Communications Officer position

2 hours -

Kingsley Quiz Competition produces 20 Cuba-trained medical doctors for Ghana

2 hours -

Police arrest alleged motorbike theft syndicate, recover 17 suspected stolen bikes in Upper West

2 hours -

Culture before internal communication: Why Africa needs the Accra Framework

2 hours -

12-year-old girl dies as rainstorm destroys over 40 homes in Yendi

2 hours -

Africa’s next economic frontier will be built from already accumulated knowledge

3 hours -

Airtel Africa dials up London for mobile money IPO

3 hours