Audio By Carbonatix

Heath Goldfields announced its first gold pour on 19th February 2026. The mine had been dormant for two years. Fourteen hundred workers, the company said, were back on payroll. The Trafigura offtake agreement for 700,000 ounces of gold doré, with $65 million in debt financing, followed within weeks. Bloomberg picked up the story for the world’s mining capitalists.

On the surface, it sounds like the kind of story Ghana now wants to hear in its mining sector. A locally owned firm restarting a historic mine, attracting world-class commodity finance, and doing so against the backdrop of a gold rally that has pushed prices past $5,000 an ounce, the most furious ascent since the late 1970s.

Ghana, the continent’s largest gold producer, has found its homegrown swagger, and the citizens are loving it.

But the story beneath the pour is a different one entirely. Scratch the surface lush, and the Heath Goldfields saga reveals something totally crazy. It is the perfect case study in how African countries, even amid generational commodity booms, manage to convert geological fortune into chronic failure.

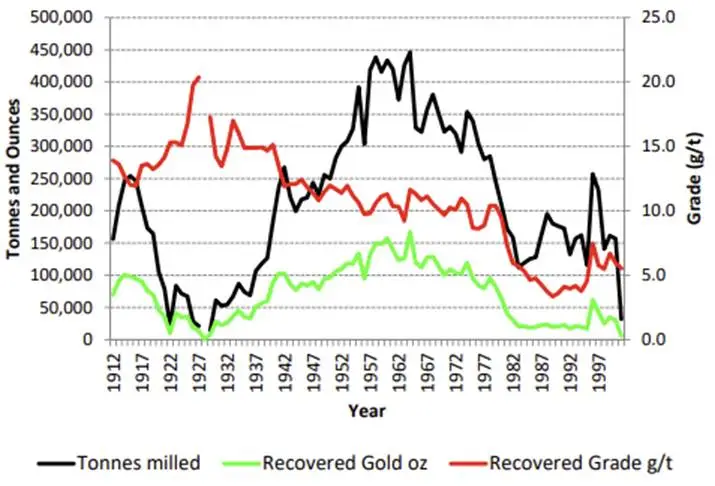

The mine at the centre of it all, Bogoso-Prestea, has produced over nine million ounces of gold since 1912. Yet it remains, in 2026, a monument to squandered opportunity.

Every company that has touched it has either walked away bruised or been forcibly removed. What at all is going on? Why can’t Ghana build its own Newmont? Why isn’t Obuasi brimming with skyscrapers? Why doesn’t gold leave the same shiny residue it left about San Francisco? Is it simply just because foreigners have sucked away all the juice and left the pulp behind? Even if so, why does Ghana continue to allow it?

Nine Million Ounces and Counting

Bogoso-Prestea sits on the southern end of the Ashanti Greenstone Belt, a 250-kilometre geological corridor of Paleoproterozoic rock that is, by any measure, one of the planet’s most fertile gold-bearing structures. The belt hosts Obuasi, Tarkwa, Wassa, and Damang.

Prestea alone has been mined since at least the 1870s, first by European prospectors, then by Ariston Gold Mines from 1912, which sank the shafts and developed the underground workings that still define the site.

After a turbulent period of state consolidation and divestment, production at Bogoso – Prestea plummeted to just a little over 20,000 ounces in 1984 under state control.

Yet, taking the full span of its history into account, the Bogoso-Prestea mining enclave is the stuff of rich pickings.

In the early 1960s, the Government of Ghana bought the assets of the various companies along the belt and formed the Prestea Goldfields with limited liability under the Ghana State Gold Mining Corporation (SGMC).

Peak annual production hit 167,000 ounces in 1964, at an average recovered grade of 11.6 grams per tonne. In the underground passages below the town of Prestea, the West Reef’s fault-fill quartz veins have yielded grades exceeding 100 grams-per-tonne in individual channel samples.

These are the kinds of numbers that international mining bosses drool over. A 2017 technical report estimated 5.1 million ounces of gold could still be stashed in the Bosogo-Prestea mining enclave. The technical folks say that the underground reserves have grades of 8.1 grams-per-tonne and that metallurgical recoveries of 94 per cent through carbon-in-leach processing is possible.

The site has two functioning shafts, a 1.5 million tonne-per-annum CIL plant, and a separate BIOX® sulphide processing circuit. On paper, Bogoso-Prestea is indeed the kind of mine that junior explorers spend decades dreaming about finding. In practice, it has eaten its owners alive.

Nationalised in the late 1950s after independence, consolidated under the State Gold Mining Company, then reopened to foreign investment in the 1990s after poor management left it bony and lanky, the mine has cycled through Barnex JCI, Prestea Gold Resources, and eventually Golden Star Resources, the Canadian firm controlled by billionaire Naguib Sawiris that acquired the Bogoso concession in 1999 and the Prestea underground in 2001.

Golden Star invested quite a bit: refurbishing shafts, installing ventilation systems, commissioning BIOX® technology, and deploying the Alimak mechanised shrinkage mining method. Yet by 2019 the company had written down the mine’s value by $56.8 million, leading to a net annual loss of $78 million.

The underground segment of the mine had never delivered consistently, owing to geological complexity, the nuggety grade distribution of the West Reef, and recurring water ingress into deeper levels.

When Golden Star announced the sale of Bogoso-Prestea to Future Global Resources in July 2020 for up to $95 million, it was framed as a win for everyone. FGR, the London-based newcomer, would bring “fresh focus and investment.” Golden Star would concentrate on Wassa. Yet the payment structure hinted at a bit of desperation on Golden Star’s part.

Just $5 million upfront, $10 million due in 2021, and a further $15 million in 2023, plus a contingent payment of up to $40 million pegged to the sulphide project. It was a sale on instalments, designed to defer the pain. The pain came anyway.

London Calling, Accra Fumbling

FGR was, by any standard measure, an unusual acquirer. Incorporated in December 2019 as a subsidiary of Blue International Holdings, it was a vehicle co-founded by Andrew Cavaghan and Mark Green, professional investors with financial pedigree but no mining experience.

Blue International’s portfolio included Joule Africa, a renewable energy developer. Its advisory board featured Lord Dannatt, the former head of the British Army; Lord Triesman, a former Foreign Office minister; and Philip Green, who was rebuilding his reputation after the collapse of Carillion.

A Guardian’s investigation later revealed the full tapestry of entanglement. John Glen, a UK Treasury minister from 2018 to 2023, held shares in Blue International. The UK’s Future Fund had lent the company £3.3 million of taxpayer money. Devonport Capital, a lender specialising in high-risk jurisdictions and run by Paul Bailey with Thomas Kingston, a Foreign Office veteran married to Lady Gabriella Windsor, had extended roughly $5 million to Blue International.

When the Ghanaian venture began to unravel, Devonport’s own creditors, including the Legatum Group’s founder Christopher Chandler and the British tax agency, were pulled into the maelstrom. Kingston died in February 2024. Devonport entered administration a year later, with creditors owed £49 million and recovery estimates as low as £11.2 million.

In Ghana, FGR’s tenure was marked by repeated shutdowns, unpaid wages, and accumulating supplier debts. Abdul-Moomin Gbana, General Secretary of the Ghana Mineworkers’ Union, described communities around the mine becoming “virtually ghost towns.” FGR also struggled to pay Ghana’s state electricity company.

Workers protested with brass bands and placards reading “Blue Gold is a scam.” Yet FGR’s parent restructured the asset into Blue Gold, listed it on NASDAQ via a merger with a blank-cheque firm, and announced it had secured $140 million in restart financing with $65 million held in escrow. But the money seemed stuck somewhere between New York, London, and the mine.

Blue Gold’s NASDAQ stock crashed 96.86 per cent from its peak. The company recorded no revenue, a $15.1 million annual loss, and a working capital deficit of $10.7 million.

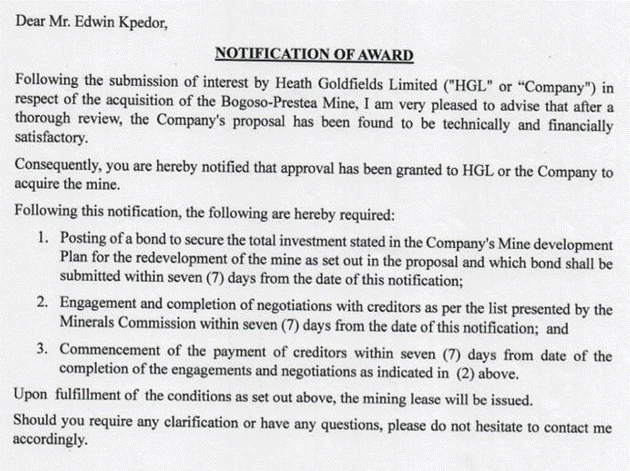

It was into this seeming vacuum that Heath Goldfields materialised like a rabbit out of a hat. The company was incorporated on 6 February 2024 with a stated capital of GH¢10,000, roughly $700. One week later, on 13 February, it applied for the mining lease, even though the lease was still legally held by FGR/Blue Gold. By September 2024, the Minister of Lands and Natural Resources had terminated the previous lease.

By November, the Minerals Commission had approved the reassignment to Heath Goldfields. Four days after a letter ostensibly suspending the process, Heath personnel had, according to various accounts, mobilised to site, to assert control over vehicles, residential assets, and gold stockpiles.

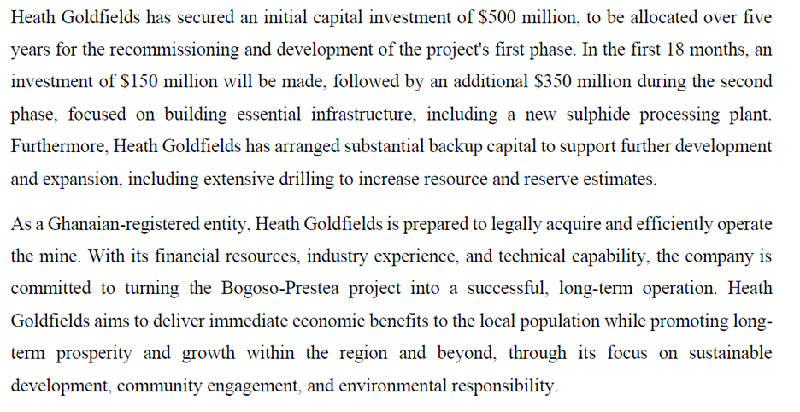

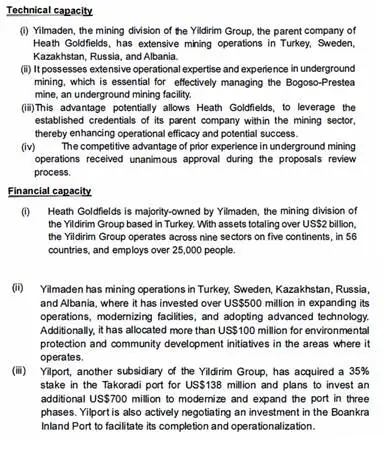

Who stood behind Heath Goldfields? The initial presentation to the Minerals Commission described the company as a subsidiary of the Yildirim Group, a major Turkish conglomerate whose mining arm, Yilmaden, operates across several countries. A promise of $500 million in investment was stated in the strategic plan accompanying the proposal.

On the strength of these claims, or more likely the relationships, the award of leases followed.

But soon trouble reared its head. The Catchment Area Community Alliance, a local youth group, subsequently petitioned the government, noting that publicly available information on the Yildirim Group’s corporate structure does not list Heath Goldfields among its recognised entities.

This is extremely strange as the Bosses at the Minerals Commission had told the Minister in their October 23, 2024, letter that Heath is indeed owned by the Yildirim Group. Plus, a host of other credentials and commitments.

The promised half-billion dollars has not materialised. None of the Minerals Commission bosses who told the Minister that Heath is a subsidiary of the Turkish conglomerate has ever been questioned. When it became clear that the Turkish funds won’t come, a new list of financial sponsors started to circulate.

Source Amount

Shareholder loan $30 million

Trafigura financing $65 million

ECOWAS Bank for Investment & Development $100 million

First Atlantic Bank $5 million

Guaranty Trust Bank $6 million

Months afterwards, the cash pipeline seemed dry. The recent announcement of the Trafigura offtake together with $65 million in debt financing would thus appear to be the only one in the latest of promises to be redeemed. While significant, it comes nowhere close to the original aggregate pledge.

What has now become quite clear, following amendments to the original corporate registration documents, is the domestic political machinery behind the venture.

Dr Kwabena Duffuor, a former Minister of Finance and one of Ghana’s wealthiest individuals, is a director. His son, Dr Kwabena Duffuor Jnr, serves as Board Chairman.

Directors and corporate secretaries listed in early filings include Sylvia Naa Odarley Amporful and Edwin Kpedor, a lawyer whose name appears on multiple company documents. Eureka Capital, an entity mentioned in other disputes involving the Duffours and an industrialist about a packaging factory, also features.

The Turkish connection, presented as the backbone of the venture’s technical and financial credibility, has vanished like morning mists at noon.

Since assuming control, Heath Goldfields is reported to have dismissed over 400 workers, citing “operational restructuring.” Those workers subsequently held a press conference accusing the company of deceit, discrimination, and financial neglect.

Only partial payments of salary arrears have been made. Severance packages, provident fund contributions, bonuses, and repatriation entitlements remain largely outstanding, according to worker representatives.

A GH¢136 million settlement was later announced, but verification of its completeness remains disputed. Ruling party executives have demanded termination of the lease and reassignment to a more capable investor.

Even local chiefs have jumped on that bandwagon. The confusion has led to questions about whether the company possesses the technical competence and financial depth to sustainably manage one of West Africa’s most complex gold operations.

Trafigura’s Calculated Bet

The April 2026 Trafigura offtake merits particular scrutiny, less for what it says about Trafigura than for what it reveals about the desperation of the Heath Goldfields position. Trafigura is a $244-billion-revenue commodity trader that has spent two decades expanding its metals and minerals footprint across Africa.

The $65 million in debt financing it is extending is secured against a stream of 700,000 ounces of gold. At current prices just south of $5,000 per ounce, those ounces carry an aggregate market value approaching $3.5 billion. Trafigura’s exposure is, by its own portfolio standards, trivial. What it gains is a locked-in physical supply from a producing asset at a moment when gold is the most coveted commodity on the planet.

For Heath Goldfields, the deal appears to be its only lifeline. Without external financing, the restart of even the oxide operations is unachievable. The underground levels of the mine remains badly flooded well above the 18th Level, with installations between the 18th and 24th Levels, including locomotive trains, power stations, and ore passes, fully submerged.

Rehabilitating the underground segment to the point of productive mining would require capital expenditure measured in the hundreds of millions, not the tens of millions that Trafigura’s facility provides.

The Trafigura deal, impressive as its headline numbers sound, may finance stockpile-processing and limited surface-mining operations, but that is far from the reinvigoration needed.

Heath’s hopes are that the deal might trigger more inward investment from other parties. But there are serious concerns about the regulatory tightness of the arrangement.

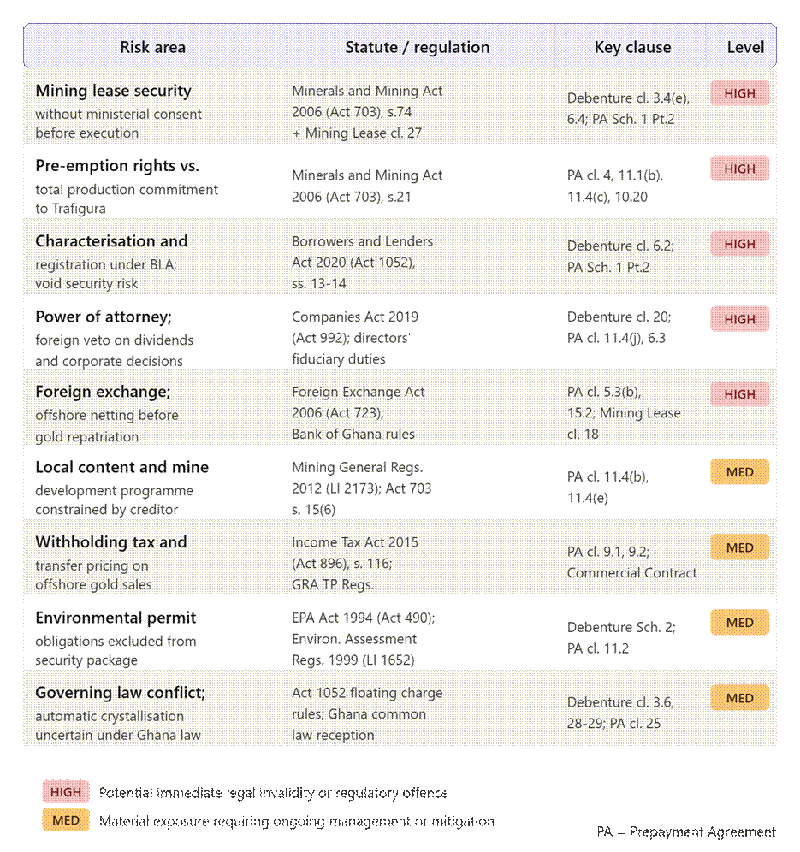

Did Trafigura Look Before it Leaped? Or Was it Assured by Powers That Be?

Clause 3.4(e) of the April 2, 2026, Trafigura-Heath Debenture assigns, by way of first priority security, Heath Goldfields’ three mining leases (APL-M-147, APL-M-148, and APL-M-149, all dated December 13,2024, to Trafigura.

This is softened by the “Effective Date” definition in Clause 1.1.12, which defers the mining lease security to the “Consent Date” – the date the Minister for Lands and Natural Resources issues a no-objection letter. Clause 6.4 gives Heath Goldfields 60 days to procure that consent.

The problem is that section 14 of the Minerals and Mining Act, 2006 (Act 703) prohibits the creation of any encumbrance over a mining lease without PRIOR ministerial consent. The agreement between Heath and Trafigura has, however, already been executed, signed, and in force.

Even where the security’s effectiveness is contractually deferred, the legal question is whether the executed assignment instrument itself – drafted in terms that create a contingent proprietary interest – constitutes a disposition requiring consent before execution rather than after.

Section 21 of Act 703 (Ghana’s main mining law, twice amended) vests the Government of Ghana with a right of pre-emption over minerals produced from mining concessions. Clause 10.20 of the Trafigura – Heath Prepayment Agreement formally acknowledges this right.

However, Clauses 4 and 11.1(b) require Heath Goldfields to maintain an Offtake Coverage Ratio of at least 200% at all times, effectively committing all current and future production to Trafigura’s offtake. Clause 11.4(c) prohibits any new prepayment or pre-export financing that might affect this commitment.

Local Ownership Doesn’t Always Mean Local Control

Another lesson that comes out strongly from the Trafigura offtake agreements is the divergence between local ownership and control, especially if the “local champion” is weak. Clause 11.4 of the Prepayment Agreement gives Trafigura veto power over dividends, share redemptions, management fees, capital expenditure on sulphide ore, corporate restructuring, change of control, and any new financial indebtedness.

The aggregate effect is that a Singaporean commodity trader holds effective operational and financial control over a Ghanaian mining operation even though a local company fronts “ownership”.

The separate Ghanaian Law Share Charge pledges the shares of Heath Goldfields held by Eureka Capital to Trafigura. On enforcement, Trafigura would acquire de facto control of a Ghanaian mining company holding three active mining leases.

A change of ownership of this kind would normally require ministerial consent under Act 703 but the legal documents are vague about what happens if that consent is not forthcoming. It is also vague if Ghana’s forex laws are respected in the payment model adopted for overseas net-offs of proceeds against debt obligations when Heath delivers gold to Trafigura.

Blue Gold Fumes in the Background

Meanwhile, Blue Gold’s international arbitration under the UK-Ghana bilateral investment treaty proceeds at the Permanent Court of Arbitration in The Hague, seeking damages estimated in excess of $1 billion. If Blue Gold prevails, the financial consequences for Ghana could be severe, potentially exceeding the entire revenue the mine might generate under Heath’s stewardship.

If it fails, the precedent will chill future foreign investment regardless, because the spectacle of a NASDAQ-listed company being stripped of its asset and replaced by a company incorporated one week earlier with $800 in capital is not a story that institutional investors forget.

Jurisdictional Chaos is an Industry Disease

The chaos at Bogoso-Prestea is chronic and reflects systemic conditions. Ghana’s mining sector and, more broadly, the resource governance of many African states, are constantly trapped in this kind of confusion.

I think it is fair to characterise the situation as chronic jurisdictional chaos: a variant of the general katanomics I regularly rail against. The chronic misalignment between the regulatory system, the political incentives, and the commercial realities of mining are legion.

Every actor in the Bogoso-Prestea saga, from Golden Star to FGR to Heath Goldfields, has operated in an environment where the rules appear to bend depending on who is applying pressure, where tenure is precarious regardless of legal formality, and where the government’s role oscillates between regulator, landlord, equity partner, and political dealmaker.

Consider the sequence of events at Damang, another mine in the same belt, where a 7-day tender window was created for a mine requiring $500 million in investment, a bankable feasibility study, environmental impact assessments, and water-use permits.

In both the Damang and Bogoso-Prestea cases, the regulatory process was compressed to the point where only insiders could navigate it. In both cases, the financial and technical prerequisites for responsible mine operation were warped by political fiat.

I would like to submit that this is not resource nationalism. Resource nationalism, done competently, is what Chile achieved with Codelco and what Botswana built with Debswana. It is not possible to grow “national champions” on soils poisoned by chaos and disorganisation.

The process of effective seeding of national champions requires the state to first establish jurisdictional quality, a predictable, transparent, and enforced legal regime, and then to leverage that quality to extract maximum value for its people using the strategically groomed national champions as instruments and vehicles.

Recent developments would appear to suggest that Ghana is doing the reverse: degrading jurisdictional quality in the hope that national champions will emerge from the chaos. What emerges instead is a revolving door of under-capitalised operators, escalating legal disputes, idle workers, and flooded mineshafts.

China’s technology sector offers an instructive parallel if Ghana’s political elite are minded to learn. When Beijing wanted to build national champions in telecommunications, semiconductors, and electric vehicles, it did not begin by expropriating foreign operators and handing their factories to politically connected entrepreneurs.

It began by establishing industrial zones with predictable rules, offering long tax holidays to foreign firms willing to transfer technology, building a massive base of trained engineers through state-funded universities, and then, over two decades, nurturing domestic firms within that ecosystem until they were strong enough to compete on their own merits.

Huawei began as a reseller of imported telecom switches. Samsung, Korea’s national champion, started as a grocery trading company and dried fishmonger. Neither was catapulted into industry leadership by regulatory fiat.

The lesson from these examples, and from the UAE’s financial services development and aviation success story, from Chile’s copper discipline, and from Indonesia’s nickel downstream policy, is that effective sequencing, rather than sentiment, does the trick.

The first step is always jurisdictional cleanup: clear rules, consistent enforcement, credible arbitration, and a regulatory culture that treats all investors, foreign and domestic, with equal rigour. Only after that foundation is set can the state then credibly favour domestic firms.

Because only then will those firms be tested by genuine competition, rather than sheltered by bureaucratic caprice, and thus build the profile able to attract better terms from business partners worldwide than the hamstringing ones that Trafigura has heaped on Heath, for instance.

Ghana seems to be exhibiting the inverse pattern when it comes to its natural resource (especially mining) sector. As the katanomics framework describes, political clarity abounds: Ghanaians overwhelmingly support greater domestic ownership of their mineral wealth.

The political class rides this sentiment with rhetorical flourish. But policy savvy, the granular, technocratic capacity to translate sentiment into sequenced, executable strategy, is conspicuously absent.

What we often see instead is “buga-buga” governance: brash, poorly thought-through interventions that achieve the appearance of nationalist victory while continuing the old pattern of chronic failures.

Bogoso Prestea keeps devouring its owners

Amidst all the chaos and noise, we have a pattern. Every operator of Bogoso-Prestea since the colonial era has encountered the same fundamental challenge: the geology is generous but complex, the underground shafts are deep and wet, the surface oxides are increasingly exhausted, and the sulphide resource, which constitutes the bulk of the remaining mineral inventory at 1.76 million ounces of measured and indicated resources, requires processing technology and capital intensity that very few operators can sustain.

The BIOX® plant, which Golden Star built to treat refractory sulphide ore, operated for years but was eventually closed due to underperformance and cost escalation. The Prestea Underground area has flooded and been dewatered and flooded again, a cycle as rhythmic and pitiless as the tropical rains that feed the aquifers.

So, what kind of operator can succeed at Bogoso-Prestea? The evidence suggests it requires deep pockets, patient capital, world-class technical management, and, crucially, a thoughtful and predictable policy and regulatory environment in which long-term investments can be made without the risk of capricious political actions. In other words, the kind of operator that jurisdictional chaos systematically repels.

The companies that venture into Bogoso-Prestea tend to share a streak of adventurism: they are startups, turnaround specialists, or politically connected entrepreneurs rather than established mining companies or top-tier startup teams covering all the key functions one needs to venture effectively into mining. It is selection bias produced by an environment that is, to put it plainly, too risky for the cautious and too tempting for the reckless.

A Golden Moment, Squandered

All of this unfolds against the most favourable macroeconomic backdrop for gold mining in half a century. Gold prices surged 42 per cent in 2025 alone, driven by central bank accumulation, geopolitical turbulence, and dollar weakness.

Global gold production margins have widened to record levels, with S&P Global estimating all-in sustaining cost margins of roughly $2,800 per ounce for 2026. African producers, from West African Resources in Burkina Faso to Allied Gold in Ethiopia, are racing to bring new ounces to market. Across the continent, the African Mining Vision’s long-standing call for greater local value retention from mining has acquired fresh urgency and plausibility.

Ghana, sitting atop one of the world’s richest gold belts as Africa’s largest producer, should be the primary beneficiary. Instead, two of its most significant mining assets, Bogoso-Prestea and Damang, are mired in disputes, operational limbo, and legal proceedings that could take years to resolve.

Despite their bad rap, it is the large, foreign-owned operations at Tarkwa, Obuasi, and Wassa, that seem likely to remain on the scene once the hysteria fades.

Despite the small-scale sector now generating half of all gold exports, few companies in that segment are being systematically supported to grow and take over mature concessions.

Bogoso-Prestea has lessons for Africa

Bogoso-Prestea carries lessons far more poignant than about troubled mining. It is a literal parable about the distance between aspiration and execution in Africa’s resource governance. The mine’s century of production, its nine million ounces of extracted gold, its 5.1 million ounces still in the ground, should represent a formidable platform for sovereign wealth creation.

That it does not, that the mine in 2026 is processing stockpiles under a company incorporated with $800 while a $1 billion arbitration looms, is an indictment not of any single actor but of a system that privileges short-term political manoeuvre over long-term institutional construction.

The deeper lesson is for Ghana and for every African country watching the global gold rally with hungry eyes. Owning your natural resources is a precondition for development, but it does not substitute for policy savvy. Between ownership and value creation lies the unglamorous, technically demanding, institutionally intensive work of building a mining sector that operates at the frontier of global practice.

That work begins with jurisdictional quality, and jurisdictional quality begins with treating every mining licence, every tender process, every lease termination, as an act that the entire world is watching and evaluating. Because in 2026, the world very much is.

The Situation is Dire

Heath Goldfields, and their formidable patrons, the Duffours, are pulling out all the stops even as calls rise from every corner for the lease to be terminated. But success at Bogoso-Prestea would take more than entrepreneurial aggression or mere political fiat.

The Chief Inspector of Mines, Richard Adjei, was emphatic in his August 2025 assessment that the continued accumulation of stagnant water underground violates Regulation 178a of LI 2182. Everyday this continues, the law is being wantonly broken. It is not clear how the company can retain a mining operating permit if the Chief Inspector’s findings remain unremedied.

The Tailings Storage Facility demands emergency intervention (you will recall from my earlier piece on Damang that there is a similar risk there too). Cells 1 and 2 carry no available freeboard – a direct breach of Regulation 264(o) and (p) – and construction on Cell 2 and Cell 2A has stalled for over a year due to unpaid contractors. Downstream communities including Dumasi and Bogoso sit in the flood shadow of a potential dam failure.

On the operational front, the sulphide plant commitment made by Heath is unlikely to met considering that the Trafigura agreement specifically constrains investment without the Swiss commodities trading giant’s prior approval.

Meanwhile, the Turkish Yilmaden Holdings investment of $500 million which was the primary basis of approval has all but disappeared from the record. According to the terms of the lease, creditor liabilities were to be extinguished within seven days. Persistent reports continue to name unpaid creditors.

It is clear that the whole affair is a total mess. It is also clear that the government must put forward a comprehensive new strategy involving the establishment of a special investment vehicle that the parties that have developed some residual interest – Blue Gold and Heath Goldfields – would become minority interest holders in exchange for dropping their operatorship expectations and all other claims.

Once this complex understanding is reached, the path would then be open for a truly competitive process to select a top-tier consortium to own majority of the structure, manage the leases, and operate the mine.

A mine of this vintage and mineral complexity – refractory ore deposits, ageing underground infrastructure, a sulphide processing gap that has persisted for years – genuinely requires an operator with capital depth and technical seriousness.

Nine million ounces have already left the ground at Bogoso-Prestea. Five million more remain. Whether those ounces enrich Ghana or merely pass through it on their way to Swiss refineries and London vaults will be determined by something more buoyant than gold prices. Another price matters more: the cost of persisting on the path of katanomics.

So far, the invoice is long and the payments are short.

Latest Stories

-

Four foreigners, three Ghanaians arrested in illegal mining raid along Boin River

5 minutes -

Gov’t procures 24,534 medical equipment ahead of free healthcare rollout

7 minutes -

NSA trial: High Court grants requests for bail variation by lawyers of Osei Assibey

8 minutes -

Workshop on human trafficking ends with call for stronger collaboration and enforcement

12 minutes -

High Court adjourns GH¢431.8m NSA fraud case involving Osei Assibey Antwi

28 minutes -

Tema Shipyard reclaims regional edge with 55% growth, renewed confidence

30 minutes -

Prioritise public education on legal aid to support vulnerable persons – Presbyterian University VC

45 minutes -

Kurt Okraku commiserates with Berekum Chelsea after fatal armed robbery attack

46 minutes -

78% of NDC delegates worried about jobs, but majority remain optimistic – Global InfoAnalytics poll

50 minutes -

Traceability is the new currency of global cocoa Trade

53 minutes -

Asiedu Nketia holds lead in NDC race but Ato Forson closing gap fast – Poll

1 hour -

Collaboration across sectors key to tackling MoMo fraud — MobileMoney Ltd CEO

1 hour -

President Mahama commends Catholic Church for role in Ghana’s development

1 hour -

Canadian PM Carney on verge of Liberal majority gov’t as votes cast in three by-elections

1 hour -

UK could adopt EU single market rules under new legislation

1 hour