Audio By Carbonatix

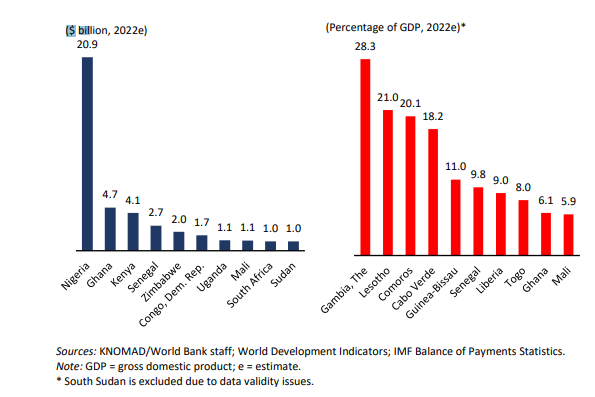

Ghana maintained its position as the 2nd largest recipient of remittances in Africa, recording $4.7 billion inflows in 2022.

This is 4.4% more than the previous year.

According to the latest World Bank Migration and Development Brief, Ghana received the second-largest remittance inflow in dollar terms and the ninth-largest level in relation to Gross Domestic Product in Africa.

Indeed, it constituted 6.1% of GDP.

The report said remittance flows to Africa in 2021 registered a strong 16.4% increase to reach $50 billion, exceeding expectations.

The largest recipients of remittances in the region during 2022 - measured in US dollar terms - included Nigeria, Ghana, Kenya, and Senegal. However, those countries more dependent on receipts as a proportion of GDP include the Gambia, Lesotho, Comoros, and Cape Verde.

The report said relative rankings of the top 10 recipients have changed little in recent years, though the Gambia has moved up in the remittances/GDP group given the dramatic political-economy changes there in recent years.

Meanwhile, Nigeria maintained its 1st position with the largest remittance inflows of $20.9 billion in 2022, compared with the $19.2 billion recorded in 2021.

The report further said financial flows to Africa have been exceptionally volatile over the long term and continuing into the 2020s), particularly for Foreign Direct Investments and portfolio flows.

“Remittances are expected to constitute 38% of total flows in 2022, with Official Development Assistance (ODA) standing at 53%. Remittance flows to Africa have maintained secular growth of a favorable 12.5% over 2000–22, contrasted with 7% gains for FDI, and 8% for ODA”.

Remittance costs high in Africa

The report said Sub-Saharan Africa remains the most expensive region to send money to.

Senders had to pay 7.8% to send $200 to African countries during quarter 2, 2022. The average difference between the five most expensive and five least expensive corridors is astounding and significantly higher than in any other developing region.

The average cost of remitting $200 from countries in the least expensive corridors amounted to 3.4% in the second quarter of 2022. In contrast, costs for the most expensive corridors registered 25.2%.

Though intraregional migrants in Africa comprise more than 70% of all migration from or within the region, intraregional remittance costs are quite high due to the small quantities of formal flows and utilization of black market exchange rates.

For example, sending $200 in remittances from Tanzania to neighboring Uganda would have cost the migrant 35.2% in the second quarter of 2022.

Remittance outlook

The report said the risk of further adverse developments in the external environment will persist through 2023, and act to lower the pace of remittance flows to Africa to 3.9%.

Price pressures for wheat, oil, and fertilizers are likely to continue into 2023, although ebbing from peaks of the previous year.

“Food affordability and deterioration of real incomes across African states will place a damper on economic growth, while government spending on subsidies and support for farmers will widen fiscal gaps. Little easing of current account deficits is seen given continuing adjustment to the large terms of trade changes of 2022. And depreciating currencies against the US dollar will magnify the rise in import prices measured in local currency”.

The report stated that remittance outturns will depend on the balancing of the increasing needs for support from the African overseas labour force, and the availability of incomes in host countries to be remitted.

Real wages are now declining in the United States and the euro area (box 1.1), indicating the likelihood of softening remittance flows.

Latest Stories

-

Fifa scraps controversial World Cup investment plan

5 hours -

WAFCON 2026: South Africa fight back to earn dramatic draw against Côte d’Ivoire

6 hours -

We should not over-commercialise football – Eric Alagidede

6 hours -

GFA should reject FIFA’s World Cup sale proposal – Eric Alagidede

6 hours -

Ghanaian woman jailed 5 years in US for $1.6million romance scam

6 hours -

Parliament passes Energy Sector Levies Amendment Bill to tighten fuel subsidy regime

7 hours -

Unique by Design project launched to promote disability inclusion in Ghana’s fashion industry

8 hours -

Joseph Paul Amoah finishes seventh in Commonwealth Games 200m final

8 hours -

Mahama urges Dagbon Regent to preserve peace and continue late Ya-Na’s development legacy

9 hours -

RANA asks Parliament to restrict MP Yakubu Mohammed child engagements until safeguarding training is completed

9 hours -

Rights group warns against exposing schoolgirl to fallout from MP’s comment

9 hours -

Family of Bukom crash victim visits Gender Minister ahead of funeral

9 hours -

An apology is not a safeguarding policy – RANA demands Parliament’s action over MP’s comment to schoolgirl

9 hours -

Prince Adu-Owusu: The August that changed everything

9 hours -

Ato Forson announces ‘New Economy’ policy for 2027 budget, promises shift to growth-focused spending

9 hours