Audio By Carbonatix

The speed with which we criticise should match the speed with which we acknowledge success. Public debate over the Bank of Ghana (BoG)’s 2025 financial results has been dominated by a single headline: a GH¢15.6 billion loss. But that headline obscures the real story. What the Bank recorded was not an economic loss. It was the financial cost of delivering one of the most dramatic stabilisation turnarounds in Ghana’s recent history.

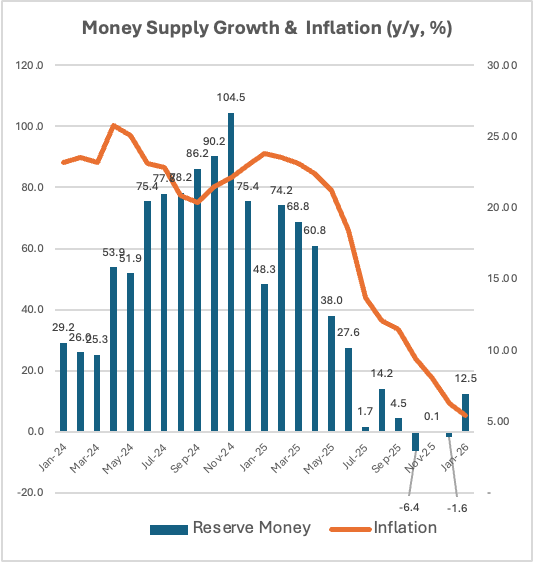

The evidence is visible in the Bank’s own data. The graph on Money Supply Growth and Inflation shows a near‑perfect mirror movement: as reserve money growth plunged from 104.5% in late 2024 to just 2.6% by December 2025. Inflation followed, falling for 13 consecutive months from 23.8% to 5.4%, and further to 3.2% by March 2026.

This is the clearest demonstration of decisive monetary policy in action.

This stabilisation was necessary because Ghana entered 2025 with a fiscal deviation of 3.1% of GDP, representing over GHS36 billion in overspending. That single slippage was equivalent to the entire IMF programme loan at today’s rates. The banking system was flooded with excess liquidity, and inflationary pressure was entrenched. The Bank of Ghana had no choice but to act. And it did.

The Loss Was the Cost of Fixing the Economy

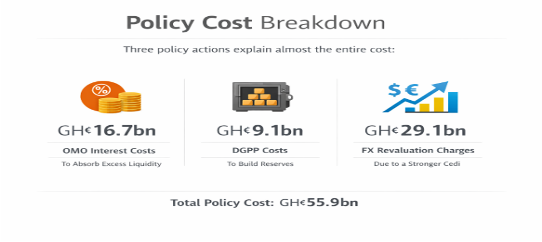

Three policy actions explain almost the entire loss:

- GH¢16.7 billion in OMO (Open Market Operations) interest costs to absorb excess liquidity;

- GH¢9.1 billion in DGPP (Domestic Gold Purchase Programme) costs to build reserves; and

- GH¢29.1 billion in FX revaluation charges due to a stronger cedi.

These are not commercial losses. They are policy costs; the price of reversing years of fiscal slippages and monetary expansion. Central banks are not profit‑maximising enterprises.

They are policy institutions. Their mandate is to stabilise prices, protect the currency, and maintain confidence in the financial system. When they act forcefully to restore stability, the financial statements reflect the cost of those actions. But the economic value created far exceeds the accounting charge.

OMO: The Weapon That Broke Inflation

OMO was the Bank’s most powerful tool. By issuing instruments to pull excess money out of the system, the Bank engineered the collapse in reserve money growth shown in the graph. Without this, inflation would not have fallen. The GH¢16.7 billion OMO cost was therefore not a loss; it was an investment and it paid off. It was also effective because fiscal managers at the Ministry of Finance maintained discipline, avoiding new slippages that would have undermined the Bank’s efforts.

The FX Revaluation Charge Was Not a Cash Loss

The FX revaluation charge has also been misunderstood. The cedi strengthened 40.7% in 2025. That strength reduced the cedi value of the Bank’s foreign assets, creating a GH¢29.1 billion accounting charge. But no reserves were lost. No cash left the Bank. The same accounting rule produced a GH¢12.7 billion gain in 2024 when the cedi weakened. The accounting treatment did not change. The exchange rate did. In simpler terms, while in 2024, every $100 on the financials was booked as Ghs1,470, the same $100 was now booked as Ghs1,045 because the cedi strengthened. The $100 remained the same but in cedi terms, Ghs425 was lost; a paper loss.

The DGPP Built the Highest Reserves in Ghana’s History

The DGPP’s GH¢9.1 billion cost must likewise be viewed alongside its outcome: reserves rose from $9.1 billion to $13.8 billion, import cover reached 5.7 months, and the programme expanded to 111 metric tonnes of gold in 2025. This was a strategic investment in resilience and ultimately contributing to the strong appreciation of the Ghana cedi by about 40%.

The Economic Gains Were Productive

The economic gains were substantial: single‑digit inflation, a 40% appreciation of the cedi, over GHS60 billion in import‑cost savings for households and firms, over GHS12 billion savings in government FX‑linked expenses, public debt falling from 61.8% to 45.3% of GDP, record reserves, lower lending rates, and renewed confidence in the currency.

The ‘Loss’ Was the Price of Stability, and It Worked

The Bank of Ghana’s 2025 loss is not evidence of mismanagement. It is evidence of a central bank doing exactly what its mandate requires: stabilising the economy, restoring confidence, and protecting the value of money.

Governor Asiamah and his deputies, Dr Zakaria and Mrs Asante, deserve recognition for the boldness and discipline that made this turnaround possible.

Senyo Hosi

Entrepreneur, Finance & Economic Policy Analyst

4th May 2025

Latest Stories

-

NDPC discusses proposed Black Star Stadium project with Western Regional Minister

34 minutes -

NDPC begins review of planning guidelines to strengthen regional and district development coordination

38 minutes -

Russia looks to students to make up for mounting losses in Ukraine

2 hours -

Argentina survive Cabo Verde scare to book Egypt date

2 hours -

Ati-Zigi, Inaki, Opoku return as Queiroz makes four changes for Colombia clash

3 hours -

MTN Ghana Awards GH¢30,000 to SME Pitch Winners.

3 hours -

48,000 displaced by Accra floods as government scales up relief operations — Mahama

3 hours -

Declare Atewa a national park now! — Eco-Conscious Citizens

3 hours -

Accra floods: Avoid politics and help those in need – Alhaji Amin appeals for corporate support

3 hours -

This Saturday on Prime Insight: Experts to dissect national flood response and Torkonoo saga

4 hours -

Ghana Sports Fund Administrator turns 10-hour US road trip into lessons for Ghana’s sporting future

4 hours -

Sentuo Group and Eezzy Foundation donate 10 ambulances and pickup vehicles to the Ghana Police Service

5 hours -

Egypt take historic step with shootout win over Socceroos

5 hours -

The Law 101 – Supreme Court upholds constitutionality in removal of CJ Torkornoo

6 hours -

Carlos Queiroz demands courage, character against Colombia

6 hours