Audio By Carbonatix

Abstract

This article explores the impact of Value added Tax (VAT) on supply of gold by Large-scale mining companies to the Bank of Ghana or Precious Minerals Marketing Company (PMMC) under the “Gold for Oil Policy” in Ghana. The author emphasised compliance with the VAT Act and made recommendations on the ways forward. In this article, reference to VAT Act means the Value Added Tax Act 2013 (Act 870) as amended.

Background

On 25th November, 2022, the Reuters online news portal reported a news item on Government of Ghana’s policy to use gold in exchange for oil. The report is quoted as saying:

“Ghana's government is planning a new policy where gold rather than U.S. dollar reserves will be used to buy oil products. The move is meant to tackle dwindling foreign currency reserves coupled with demand for dollars by oil importers, which is weakening the local cedi and increasing living costs”.

The report therefore quoted the Vice President of the Republic as saying:

“Ghana has ordered all Large-scale mining companies to sell 20% of their entire stock of refined gold at their refineries to the Bank of Ghana from Jan. 1, 2023, Vice-President Mahamudu Bawumia said on Facebook on Friday”

Given that this policy is expected to take off on January 1, 2023, there is an intriguing need to look at the crystal ball to see if there are any hidden tax issues that require attention. As said by Oliver Wendell Holmes, Jr in 1927, in his dissenting opinion in the court case of Compania General de Tabacos v. Collector, 275 U.S. 87 (1927), “Taxes are what we pay for a civilized society”. Based on Holmes statement, this author will add that taxes are what we pay to buy civilisation, peace and prosperity.

The following tax types may require attention from government in its pursuit to implement the policy. These are the VAT, Withholding Tax, Company Income Tax and Export duty. For the purpose of this article, the author focuses specifically on the implication of VAT on this policy. The author’s understanding of the policy, as quoted by Reuters is that the Large-scale mining companies will sell at least 20% of their entire stock to the Bank of Ghana.

Literature review from the National Petroleum Authority in Ghana suggests that the Bank of Ghana and the Precious Minerals Marketing Company (PMMC) are directed to coordinate the policy of the Government. In that case, it is anticipated that either the Bank of Ghana or PMMC may play an active role in this policy direction. If this is the case, then the Large-scale Mining Companies are the sellers of the gold on the one part and the Bank of Ghana is the buyer of the gold on the other part.

The scope of the VAT and its implication on the “Gold for Oil Policy”

It is important to avert our minds to the extent to which the VAT applies to this policy. VAT is applicable to all taxable activities in Ghana. This is provided for in section 1 of the VAT Act.

Section 1 of the VAT Act provides that;

“There is imposed by this Act a tax to be known as the value added tax which is to be charged on the supply of goods or services made in the country other than exempt goods or services; and import of goods or import of services other than exempt import.”

It further states in section 1(2) that

“unless otherwise provided in this Act, the tax is charged on the supply of goods or services where the supply is a taxable supply; and made by a taxable person in the course of the taxable activity of that person”.

The question is whether gold is considered as a supply of goods which is liable for taxes under the VAT Act. In this case, reference is made to what constitutes supply under section 20 of the VAT Act. In section 20, the Act provides that:

“Except as otherwise provided in this Act and the Regulations, “supply of goods” means an arrangement under which the owner of goods parts with possession of the goods, by way of sale, barter, lease, transfer, exchange, gift or similar disposition; and “supply of services” means a supply which is not a supply of goods or money, and in the nature of (i) the performance of services for another person; (ii) the making available of a facility or advantage; or (iii) tolerating a situation or refraining from doing an activity. (2) For purposes of subsection (1) (a), supply of goods does not include the supply of money.”

Section 33 of the VAT Act explains what constitutes taxable supply. It states; “except as otherwise provided in this Act or Regulations, a taxable supply is a supply of goods or services made by a taxable person for consideration, other than an exempt supply, in the course of, or as part of taxable activity carried on by that taxable person”

Moreover, section 35 of the Act explains what constitutes exempt supply. It states that exempt supply is a supply of goods and services specified in the First Schedule as an exempt supply and not subject to the tax. A supply of goods or services is not an exempt supply if that supply is subject to tax at the rate of zero percent under section 36 of the VAT Act.

Another issue is whether or not the “Gold for Oil Policy” constitutes a taxable activity in Ghana. Supply of goods is covered by the VAT Act where the taxable activity or part of the taxable activity that gives rise to the supply occurs in Ghana or the place of supply is in Ghana and the person who makes the supply is registrable under the Act.

Taxable activity in this case means an activity which is carried on by a person in the country, or partly in the country, whether or not for a pecuniary profit and involves or is intended to involve, in whole or in part, the supply of goods or services to another person for consideration. The nature of the transaction under the policy requires that the gold is supplied at the point of the refinery. This means that the gold is mined from Ghana, processed from Ghana, transported or shipped to the refinery outside Ghana. The chain of supply therefore points to the fact that part of the taxable activity for the gold transaction occurs in Ghana, thus the mining and processing of the gold. As a result, it is not in doubt that the taxable activity occurs in Ghana and for that matter, the transaction is within the scope of the VAT Act.

Further, section 42(1) of the VAT Act provides that a place of supply of goods is the place where the goods are delivered or made available by the supplier to the buyer. Moreover, where the delivery or making available of the goods to the buyer involves the goods being transported, the place where the goods are when the transportation commences is the place of supply.

In this case, where the policy requires that the gold is to be supplied at the point of refinery, and the supplier does not refine the gold at its own premises but at some other premises, it therefore requires the supplier to transport the gold to the place of refinery before the delivery occurs. As a result, transportation of the gold to the point of refinery outside the premises or the stores of the supplier before the delivery to the buyer is implicit or part of supply arrangement. The two activities should not be delineated.

The place of supply should be interpreted to mean the place where the transportation commences as provided for in section 42 (1) of the VAT Act and referred to above and not where the delivery actually occurs. This becomes more notable when both the buyer and the seller are residents of Ghana. The point of invoicing and payment actually takes place in Ghana. All these define the place and time of supply for the VAT to apply.

Gold as a taxable supply and not an exempt supply under the First Schedule of the VAT Act.

Since gold or other precious minerals are not services but goods, another critical question is whether gold is a taxable supply or exempt supply. For supply to be treated as exempt supplies, such supply must be listed under the First Schedule of the Act. As stated in section 35 of VAT Act and referred to above, supply of goods and services specified in the First Schedule are exempt supply and not subject to the tax under the Act. Therefore, one needs to look into the First Schedule to find out whether supply of gold is listed under the First Schedule to VAT Act.

A reference to the First Schedule reveals that gold is not listed as an exempt supply. As result, gold supplied will not be treated as exempt supply but rather taxable supply. The Large-scale Mining Companies supplying at least their 20% stock to the Bank of Ghana/PMMC under the “Gold for Oil Policy” must be mindful of this aspect of the law.

Is gold sold under the “Gold for Oil Policy” treated as zero rated supply?

Zero-rated supply is a taxable supply that is taxed at a zero rate if the supply is specified in the Second Schedule. It further provides that where a taxable person has applied the rate of zero percent to a supply under this section, the taxable person is required to obtain and retain the documentary proof that is acceptable to the Commissioner-General and that substantiates the person’s entitlement to apply the zero rate to the supply. Also, under the Second Schedule of the VAT Act, supplies which are made for export outside Ghana are generally considered as zero-rated supplies.

In this case, where a Large-scale Mining Company exports gold mined from Ghana, it is expected the tax rate that will apply will be zero percent. Under the “Gold for Oil Policy”, large-scale mining companies may not be required to export at least the 20% of their gold but sell it locally to the Bank of Ghana/PMMC. Therefore, it is in no doubt that when this policy kicks-off as anticipated, the 20% portion of the entire stock of the large-scale mining companies will be deemed as supplied locally to the Bank of Ghana/PMMC and will not be subject to a zero rate, especially where the supply or part of the supply originates or commences from Ghana and supplied by a person resident in Ghana to the buyer resident in Ghana.

The incidence of the VAT on supply of Gold under the “Gold for Oil Policy”

Since the supply of gold locally to the Bank of Ghana is not exempt supply nor a zero rated supply, it therefore means that the mining companies are required to charge the VAT and its accompanying levies whenever a supply is made to the Bank of Ghana or any other agency required to buy the gold in Ghana.

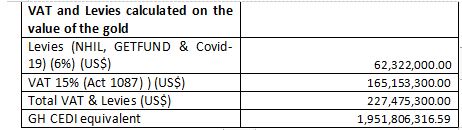

Although large-scale Mining Companies are required to charge the VAT and the Levies, the incidence of the tax lies with the recipient of the supply, in this case, the Bank of Ghana/PMMC. According to the Ghana Chamber of Mines’s 2021 mining industry statistics and data showed a total volume of gold exported from Ghana in 2021 as 79.9 metric tonnes which translated to approximately US$5.193 billion value of gold exported in 2021.

Also, according to Minerals Commission Industry Statistics for production year 2020, total income from gold was US$ 3.59 billion. Using the latest statistics from the Chamber of Mines for 2021, which pegged the total volume of gold exported in 2021 at 79.9 tonnes, this can be projected into 2023 with estimated value of US$ 5.193 billion. This means that 20% of this amount will have to be traded locally to the Bank of Ghana/PMMC. VAT is expected to be on the 20% portion of the total stock with the following VAT implications.

From the table above, the value of incidence of the tax to be borne by the Bank of Ghana/PMMC is expected to be GHS1.921 billion under the policy in its current form.

Recovery of tax from the Mining Companies by the Commissioner-General for failure to charge the VAT

The VAT Act mandates the Commissioner-General to surcharge and recover tax and collect same from a person who fails to charge VAT on taxable goods or services.

Section 55 provides as follows:

“An amount shown on an invoice or sales receipt as tax on a supply of goods or services is recoverable as tax due from the person issuing the invoice or sales receipt, whether the invoice or sales receipt is issued by a taxable person or another person, and whether or not

(a) the invoice is a tax invoice issued under this Act or in accordance with Regulations;

(b) an amount of tax is chargeable on the supply; or

(c) the person issuing the invoice is a taxable person”

So, where a Large-scale Mining Company fails to charge the tax, the Commissioner-General will be required under section 55 of the Act to surcharge and recover such amount from the Mining Company. The Commissioner-General shall also, in addition to the principal tax, recover the tax with interest in accordance with section 71 of the Revenue Administration Act 915.

Section 71 of the Revenue Administration Act, 2016 (Act 915) provides that;

“A person who fails to pay tax by the date on which the tax is payable is liable to pay interest for each month or part of a month for which any part of the tax is outstanding. (2) The interest is calculated as one hundred and twenty-five percent of the statutory rata, compounded monthly, applied to the amount outstanding at the start of the period”.

Can government exempt gold from VAT without Parliamentary approval under the Policy?

Like most countries, in Ghana, the constitutional mandate to impose or waive or vary taxes is a preserve of the legislature. The only body that is mandated to impose or waive or vary a tax is the Parliament of Ghana. This is contained in Article 174 of the 1992 constitution.

Article 174 provides:

“No taxation shall be imposed otherwise than by or under the authority of an Act of Parliament. Where an Act, enacted in accordance with clause (1) of this article, confers power on any person or authority to waive or vary a tax imposed by that Act, the exercise of the power of waiver or variation, in favour of any person or authority, shall be subject to the prior approval of Parliament by resolution”.

It is therefore clear from the above constitutional provision that; government has no such power to exempt any person from VAT unless Parliament approves such exemption. It therefore follows that government cannot, based on this directive or policy, exempt the Mining Companies from charging VAT for supplies made to the Bank of Ghana/PMMC or any other agency of government under the “Gold for Policy” unless such exemption secures a Parliamentary approval.

Author’s Recommendation

Given the significant impact that the VAT may have on both government or the Mining Companies, it is recommended that government must as matter of urgency seek Parliamentary approval for the policy by submitting a bill to Parliament under Article 106(1) of the 1992 Constitution. Article 106 provides that “the power of Parliament to make laws shall be exercised by bills passed by Parliament and assented to by the President.”

It must be further noted that, in event that government seeks parliamentary exemption from VAT, there may be further VAT implications that the mining companies will be confronted with which needs to be addressed.

Conclusion

It is evident from the foregoing that, the “Gold for Oil Policy” though laudable, the impact of VAT and other levies on this policy may derail it if the necessary steps are not taken to seek Parliamentary approval, especially on the issue of VAT. The mining companies shall be required to pay the tax to the Commissioner-General if they fail to comply with the VAT Act.

Further support

Taxpayers who require further clarification or support or education and want to seek a better approach to comply or deal with VAT and other taxation issues on this Policy or other similar issues that will affect them may contact the author or EM Tax Advisors Ltd.

****

The author, Fred Kwashie Awuttey, ESQ. is a Lawyer, a Chartered Accountant, Tax Practitioner and International Tax Advisor. He works with EM Tax Advisors as a Consultant.

He can be reached via email: info@emtaxadvisors.com, fred@emtaxadvisors.com, awuttey85@gmail.com

Website: www.emtaxadvisors.com

Mobile: +233 243 154 227

Latest Stories

-

Italy could make financial ‘exceptions’ for Guardiola

4 hours -

Villa agree loan deal for Chelsea winger Garnacho

4 hours -

Inter Miami under investigation after signing Casemiro

4 hours -

Miami mistakenly post LeBron James ‘introductory’ video

4 hours -

Saliba to miss extended period with back injury

4 hours -

Arokodare forces Wolves training to be cancelled

4 hours -

Anthony Joshua not ready for death of friends to ‘sink in’

4 hours -

CSIDT proposes 80% of GH¢350m flood budget be invested in prevention

4 hours -

US signs landmark nuclear deal with Saudi Arabia

5 hours -

Teenager drops social media addiction lawsuit against Meta

5 hours -

Trump threatens to target Iran’s bridges and power plants if Hormuz attacks persist

5 hours -

Ghana not yet in digital trust crisis, but warning signs are emerging – Kwami Tamakloe

5 hours -

Digital trust crisis looming if fraud concerns are ignored – John Awuah warns

5 hours -

Mamdani backs off pledge to arrest Netanyahu citing lack of authority

5 hours -

Banks’ NPLs drop to 16.1%, but credit risk remains key vulnerability

5 hours